Verified Documents at University of Connecticut

- Principles of Financial Accounting

- University of Connecticut

- Verified Notes

Browse the full collection of course materials, past exams, study guides and class notes for ACCT 2001 - Principles of Financial Accounting at University of Connecticut verified …

PROFESSORS

All Professors

All semesters

Suzanne Cansler

spring

28Leanne Adams

fall

39Verified Documents for Leanne Adams

Class Notes

Taken by our most diligent verified note takers in class covering the entire semester.

ACCT 2001 Lecture 1: Chapter 1 - Business Decisions and Financial Accounting

229

ACCT 2001 Lecture 1: Chapter 1 - Business Decisions and Financial Accounting

121

ACCT 2001 Lecture 1: Chapter 1 - Business Decisions and Financial Accounting

120

ACCT 2001 Lecture 1: Chapter 1 - Business Decisions and Financial Accounting

222

ACCT 2001 Lecture 1: Chapter 1 - Business Decisions and Financial Accounting

121

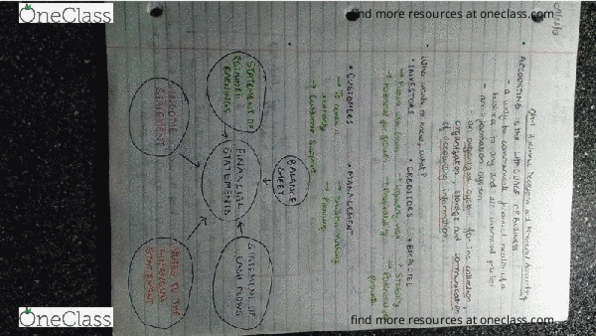

ACCT 2001 Lecture Notes - Lecture 1: Accounting, Bank Statement, Common Stock

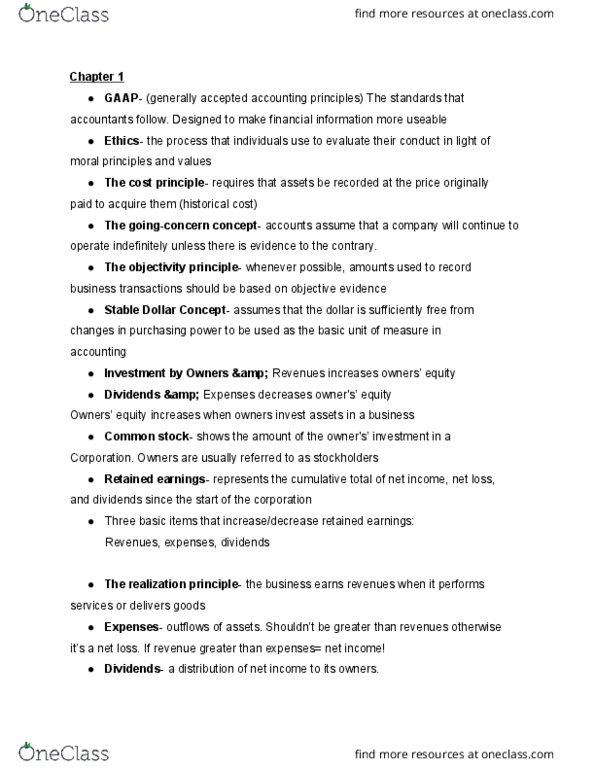

Gaap- (generally accepted accounting principles) the standards that accountants follow. Ethics- the process that individuals use to evaluate their cond

366

ACCT 2001 Lecture 2: Chapter 1 - Business Decisions and Financial Accounting

217

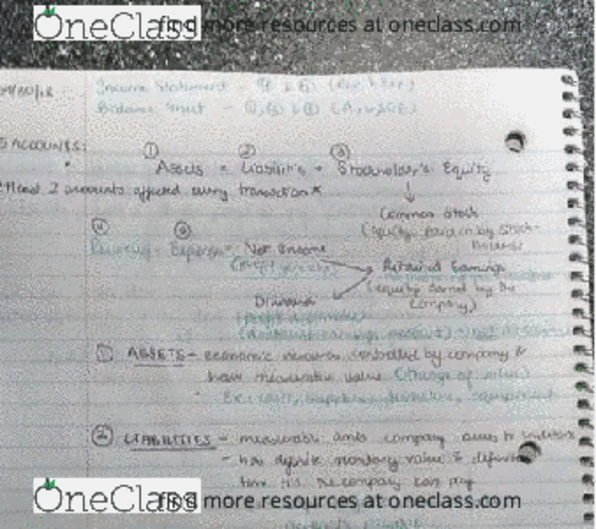

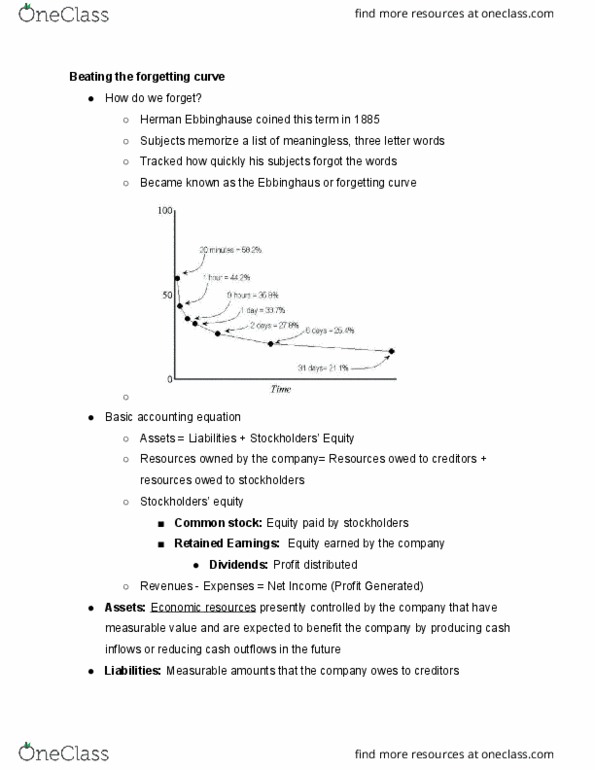

ACCT 2001 Lecture Notes - Lecture 2: Accounting Equation, Retained Earnings, Forgetting Curve

Herman ebbinghause coined this term in 1885. Subjects memorize a list of meaningless, three letter words. Tracked how quickly his subjects forgot the w

256

ACCT 2001 Lecture Notes - Lecture 3: Accounts Receivable, Accounting Equation, Accounting Information System

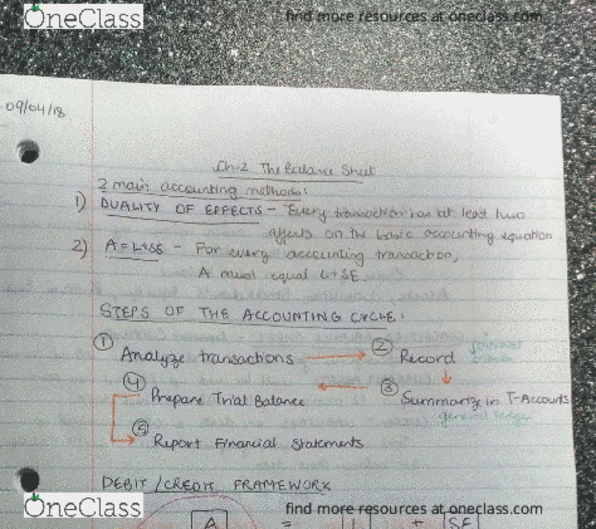

Transaction: a business activity that affects the basic accounting equation. Duality of effects: every transaction has at least two effects on the basi

260

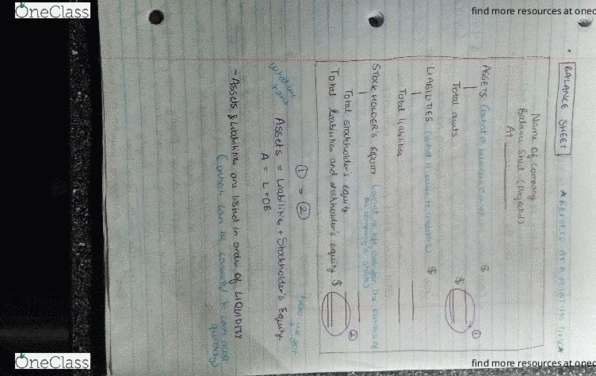

ACCT 2001 Lecture 3: Chapter 2 - The Balance Sheet

223

ACCT 2001 Lecture Notes - Lecture 4: Trial Balance, Current Liability, Accounting Equation

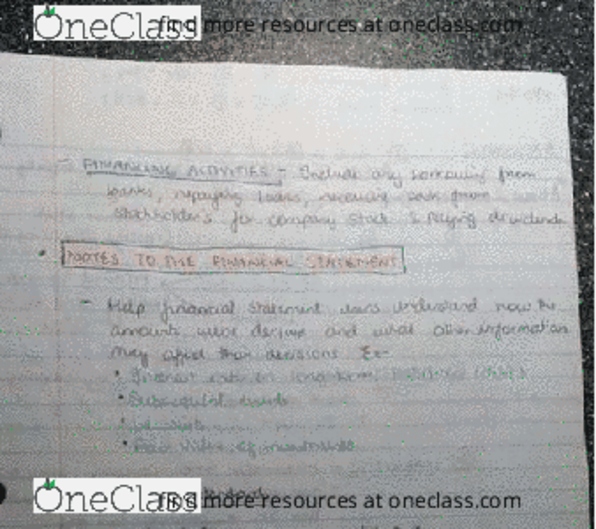

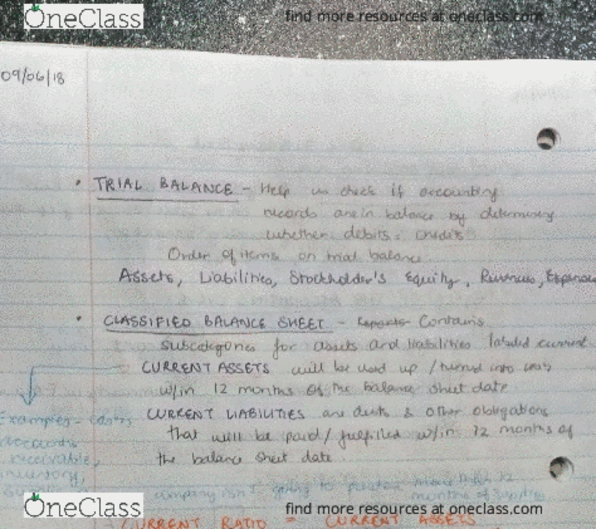

Learning objective 2-1: identify financial effects of common business activities that affect the balance sheet. Financing activities involve debt trans

381

ACCT 2001 Lecture 4: Chapter 2 - The Balance Sheet

214

ACCT 2001 Lecture 5: Chapter 3 Handout & Solution

235

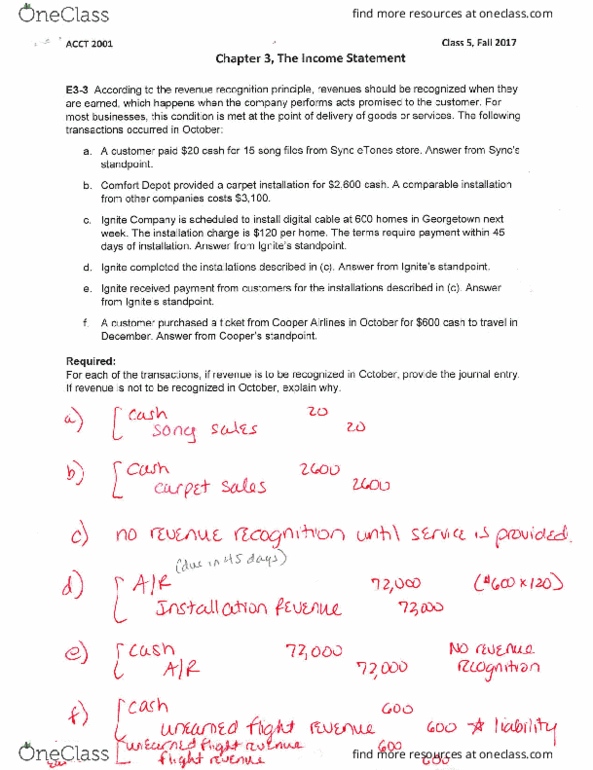

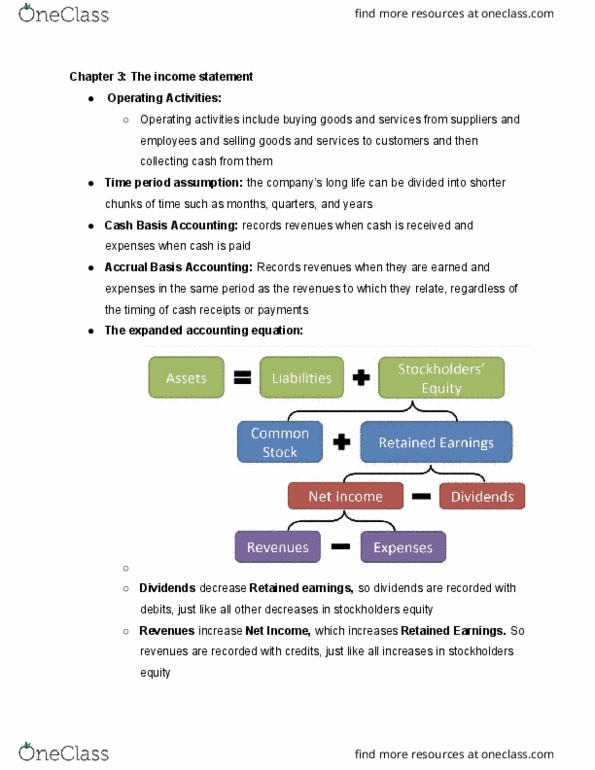

ACCT 2001 Lecture Notes - Lecture 5: Deferral, Income Statement, Accrual

Operating activities include buying goods and services from suppliers and employees and selling goods and services to customers and then collecting cas

566

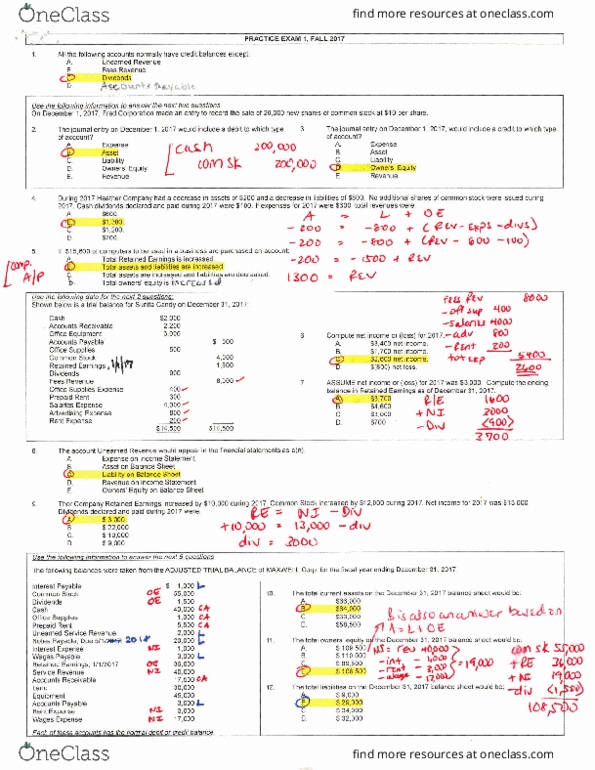

ACCT 2001 Lecture 6: Practice Exam & Solutions Chapters 1,2,3

454

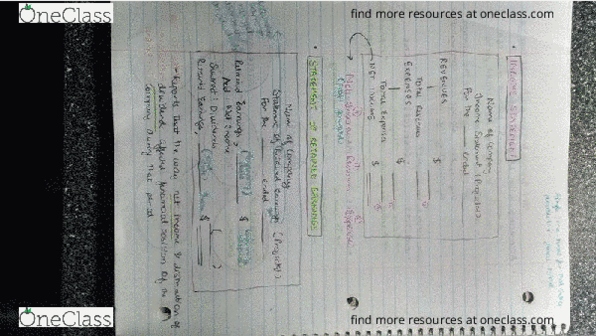

ACCT 2001 Lecture Notes - Lecture 6: Retained Earnings, Financial Accounting, Income Statement

Accounting: a system of analyzing, recording, and summarizing the results of a business"s activities and then reporting the results to decision makers.

555

ACCT 2001 Lecture Notes - Lecture 6: Profit Margin, Income Statement

146

ACCT 2001 Lecture Notes - Lecture 7: A Question Of Balance, Trial Balance, Accounts Payable

Building a balance sheet from business activities. A key activity for any start up company is to obtain financing . Two sources of financing are availa

467

ACCT 2001 Lecture Notes - Lecture 8: Accrual, Profit Margin, Net Income

Success is not final, failure is not fatal, it is the courage to continue that counts -w. c. Operating activities are the day-to-day functions involved

453

ACCT 2001 Lecture Notes - Lecture 9: Financial Statement, Trial Balance, Income Statement

Chapter 4: adjustments, financial statements, and financial results. Your comfort zone is outside of where the magic happens! Accounting systems are de

637

ACCT 2001 Lecture Notes - Lecture 10: Financial Statement, General Ledger, Matching Principle

Chapter 4: adjustments, financial statements, and financial results. The important decision you make is to be in a good mood. Analyze: determine necess

868

ACCT 2001 Lecture Notes - Lecture 11: Internal Control, Financial Statement, Mci Inc.

961

ACCT 2001 Lecture Notes - Lecture 12: Financial Statement, Whole Foods Market, Petty Cash

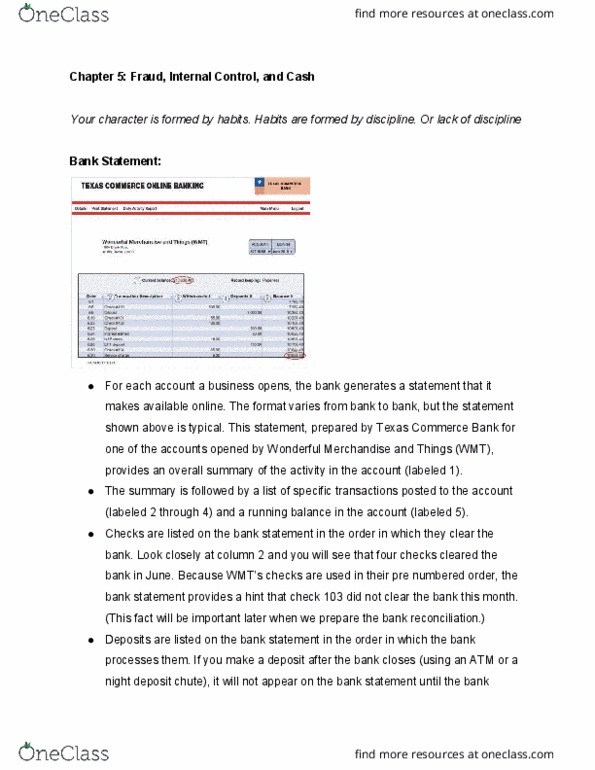

For each account a business opens, the bank generates a statement that it makes available online. The format varies from bank to bank, but the statemen

471

ACCT 2001 Lecture Notes - Lecture 13: Income Statement, Perpetual Inventory, Uptodate

471

ACCT 2001 Lecture Notes - Lecture 14: Gross Profit, Income Statement

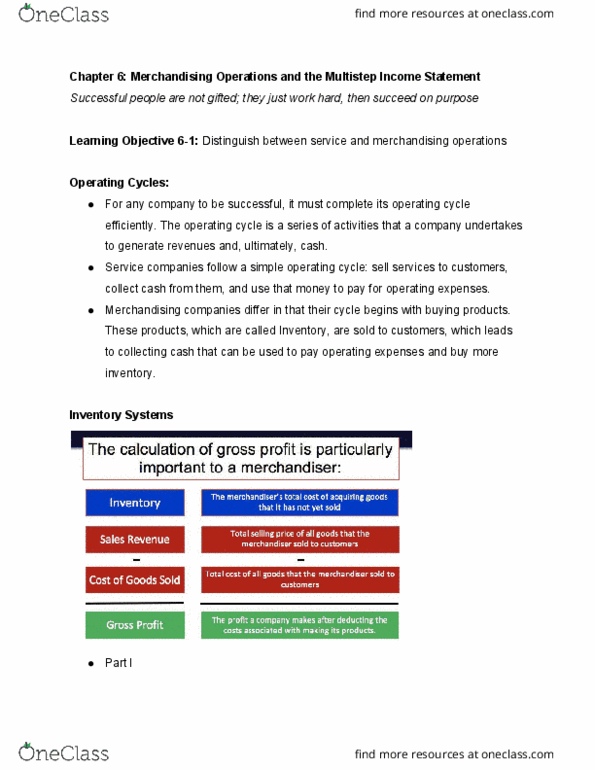

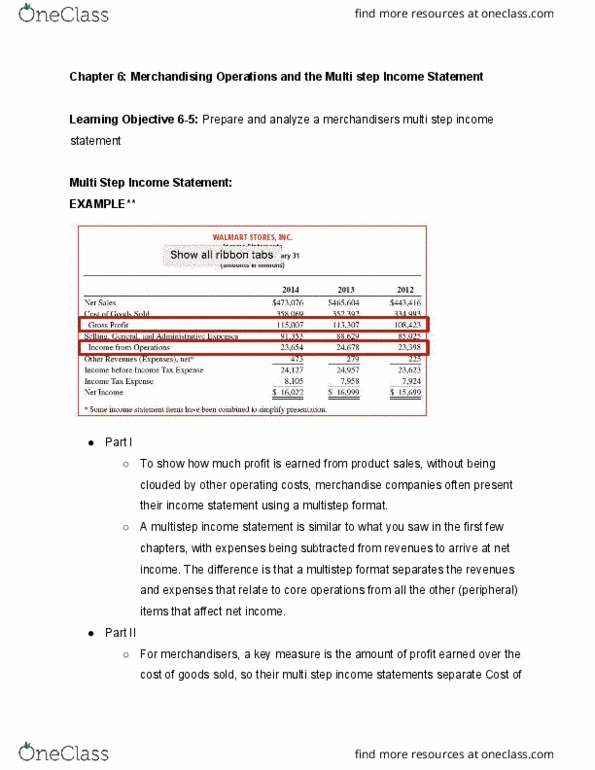

Chapter 6: merchandising operations and the multi step income statement. Prepare and analyze a merchandisers multi step income. To show how much profit

4201

ACCT 2001 Lecture Notes - Lecture 15: Retained Earnings, Financial Statement, Income Statement

Worksheet- used to bring together info needed to prepare the financial statements: does not eliminate the need to journalize/post adjusting entries, ju

4105

ACCT 2001 Lecture Notes - Lecture 16: Gap Inc., Operating Margin, Net Income

Understanding business issues: merchandising business-> earn revenue by buying goods and reselling them to customers, ex. Gap inc. , best buy, and w

2146

ACCT 2001 Lecture Notes - Lecture 17: Current Asset, Weighted Arithmetic Mean, Income Statement

Chapter 7: inventory and cost of goods sold. Learning objective 7-1: describe the issues in managing different types of inventory. The primary goals of

363

ACCT 2001 Lecture Notes - Lecture 18: Inventory Turnover, High Tech, Income Statement

Chapter 7: inventory and cost of goods sold. The pupil who is never required to do what he cannot do, never does what he can do. Learning objective 7-4

549

ACCT 2001 Lecture Notes - Lecture 19: Accounts Receivable, Accrual, Income Statement

Chapter 8: receivables, bad debt expense, and interest revenue. The advantage of extending credit is that it helps customers buy products and services,

529

ACCT 2001 Lecture Notes - Lecture 20: Promissory Note, Accounts Receivable, Matching Principle

Chapter 8: receivables, bad debt expense, and interest revenue. There are many other issues involved with bad debts and the collectability of receivabl

542

ACCT 2001 Lecture 21: Chapter 9: Long lived tangible and intangible assets

Long-lived assets are assets that are used actively in the operations of the business, and that are expected to benefit the operations into the future.

490

ACCT 2001 Lecture Notes - Lecture 22: Intangible Asset, Cedar Fair, Financial Statement

Intangible assets are normally recorded at the purchase price plus any legal or related fees. Trademarks, copyrights, patents, licensing rights, techno

379

ACCT 2001 Lecture Notes - Lecture 23: Income Statement, Accrual, Operating Expense

The oldest costs are in cost of goods sold and the newest costs are in. The oldest costs are in inventory and the newest costs are in cost of goods sol

6132

ACCT 2001 Lecture Notes - Lecture 24: Promissory Note, Weighted Arithmetic Mean, Current Asset

Understanding business issues: most businesses need to respond to changing market conditions and borrow money on a short-term basis to finance investme

1859

ACCT 2001 Lecture Notes - Lecture 27: Current Liability, Financial Statement, Promissory Note

Liabilities play a significant role in financing most business activities. 2. obtains short-term loans to cover gaps in cash flows, 3. and issues long-

574

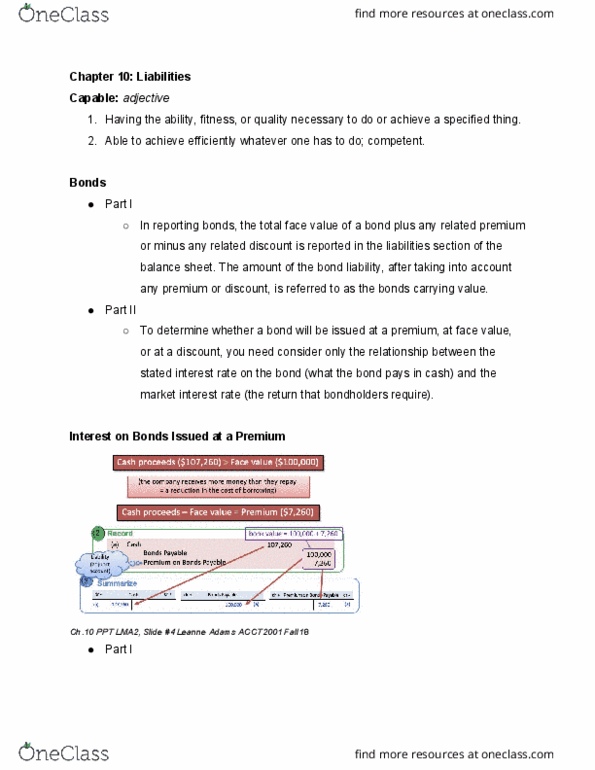

ACCT 2001 Lecture Notes - Lecture 28: Financial Statement

Adjective: having the ability, fitness, or quality necessary to do or achieve a specified thing, able to achieve efficiently whatever one has to do; co

664

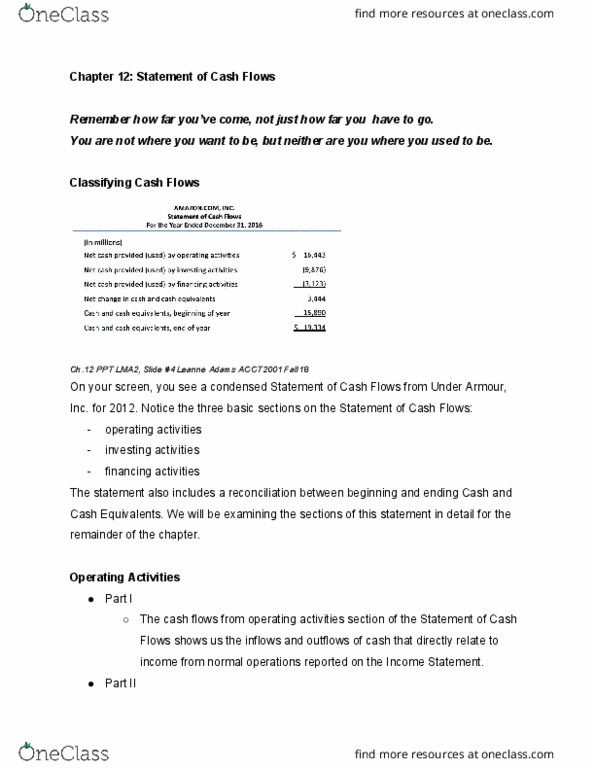

ACCT 2001 Lecture Notes - Lecture 29: Under Armour, Income Statement, Current Liability

Remember how far you"ve come, not just how far you have to go. Ch. 12 ppt lma2, slide #4 leanne adams acct2001 fall18. On your screen, you see a conden

449

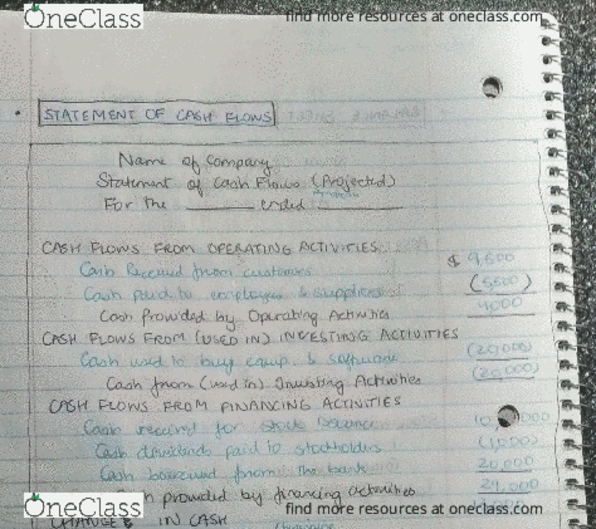

ACCT 2001 Lecture Notes - Lecture 30: Cash Flow, Income Statement, Current Asset

Cash flows from operating activities - indirect method. We will begin by focusing on the indirect method, which is used by almost all companies. The in

354