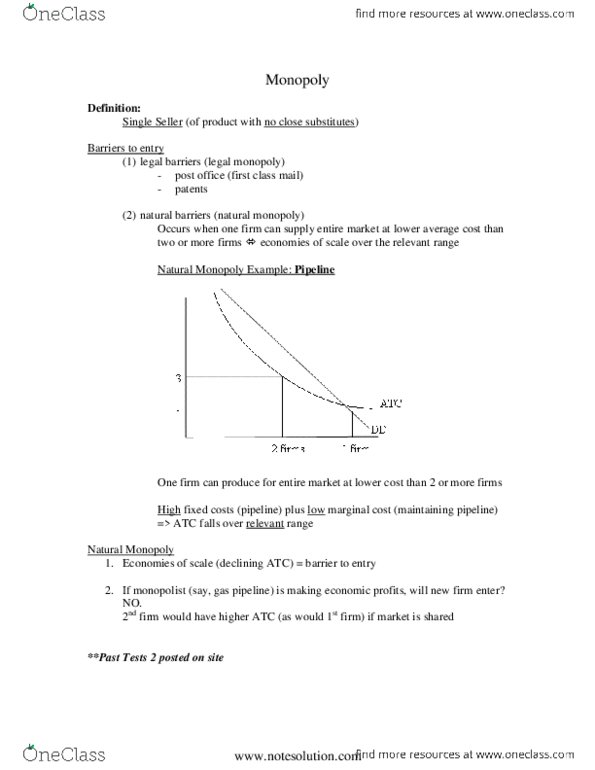

1. Patent laws:

reduce incentive to innovate by restricting market entry

reduce incentive to innovate by making it difficult to use thepatented innovation

increase incentive to innovate by restricting entry into amarket

increase incentive to innovate by giving a firm permanent andexclusive production rights

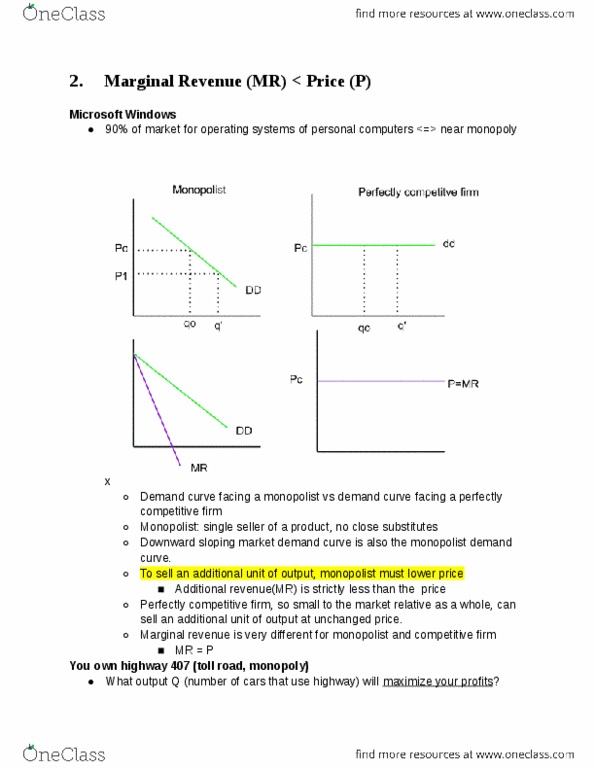

2. Which of the following is true of marginal revenue for amonopolist that charges a single price?

P = MR because there are no close substitutes for the monopolist'sproduct.

P > MR because the monopolist must decrease price on all unitssold in order to sell an additional unit.

P < MR because the monopolist must decrease price on all unitssold in order to sell an additional unit.

AR = MR because there are no close substitutes for the monopolist'sproduct.

3. Negative marginal revenue means that

total revenue is decreasing as output increases

the firm is maximizing its total revenue

the firm is maximizing its economic profit

total revenue is increasing at a decreasing rate as outputincreases

4. A profit-maximizing monopolist produces an output level atwhich

marginal revenue is the greatest distance from marginal cost

price is less than marginal cost

the value to society of the last unit produced equals marginalcost

marginal revenue equals marginal cost

5. Compared to a perfectly competitive market, a monopoly tends toproduce

more output and charge a higher price

the same amount of output, but charge a higher price

less output and charge a higher price

less output and charge the same price

6. Monopolistic competition is best described as

many firms with some control over price, and some productdifferentiation

many firms with no control over price, producing identicalproducts

a few firms with some control over price, producing highlydifferentiated products

a few firms with no control over price, producing similarproducts

7. Which of the following characteristics does perfect competitionshare with monopolistic competition?

price-taking firms

zero long-run economic profit

homogeneous product

some barriers to entry

8. Monopolistically competitive firms do not achieve productiveefficiency because

entry of firms raises production costs in the long run

barriers to entry allow profit to be earned in the long run

price is greater than marginal cost at the profit maximizing outputlevel

profit is maximized at a quantity where average total cost is notminimized

9. There are multiple models of pricing behavior in oligopolisticmarkets because

it is difficult to predict how rival firms will react to anypricing decision

the demand curve slopes upward for these firms

firms could earn profit in the long run unlike other markets

price has a direct impact on profit for a firm in oligopoly

10. Which of the following is likely to occur when a two-persongame can be played repeatedly?

Collusion and cooperation among the players

The prisoner's dilemma

The industry demand curve will become perfectly elastic

The industry demand curve will become perfectly inelastic

1. Patent laws:

reduce incentive to innovate by restricting market entry

reduce incentive to innovate by making it difficult to use thepatented innovation

increase incentive to innovate by restricting entry into amarket

increase incentive to innovate by giving a firm permanent andexclusive production rights

2. Which of the following is true of marginal revenue for amonopolist that charges a single price?

P = MR because there are no close substitutes for the monopolist'sproduct.

P > MR because the monopolist must decrease price on all unitssold in order to sell an additional unit.

P < MR because the monopolist must decrease price on all unitssold in order to sell an additional unit.

AR = MR because there are no close substitutes for the monopolist'sproduct.

3. Negative marginal revenue means that

total revenue is decreasing as output increases

the firm is maximizing its total revenue

the firm is maximizing its economic profit

total revenue is increasing at a decreasing rate as outputincreases

4. A profit-maximizing monopolist produces an output level atwhich

marginal revenue is the greatest distance from marginal cost

price is less than marginal cost

the value to society of the last unit produced equals marginalcost

marginal revenue equals marginal cost

5. Compared to a perfectly competitive market, a monopoly tends toproduce

more output and charge a higher price

the same amount of output, but charge a higher price

less output and charge a higher price

less output and charge the same price

6. Monopolistic competition is best described as

many firms with some control over price, and some productdifferentiation

many firms with no control over price, producing identicalproducts

a few firms with some control over price, producing highlydifferentiated products

a few firms with no control over price, producing similarproducts

7. Which of the following characteristics does perfect competitionshare with monopolistic competition?

price-taking firms

zero long-run economic profit

homogeneous product

some barriers to entry

8. Monopolistically competitive firms do not achieve productiveefficiency because

entry of firms raises production costs in the long run

barriers to entry allow profit to be earned in the long run

price is greater than marginal cost at the profit maximizing outputlevel

profit is maximized at a quantity where average total cost is notminimized

9. There are multiple models of pricing behavior in oligopolisticmarkets because

it is difficult to predict how rival firms will react to anypricing decision

the demand curve slopes upward for these firms

firms could earn profit in the long run unlike other markets

price has a direct impact on profit for a firm in oligopoly

10. Which of the following is likely to occur when a two-persongame can be played repeatedly?

Collusion and cooperation among the players

The prisoner's dilemma

The industry demand curve will become perfectly elastic

The industry demand curve will become perfectly inelastic

Related textbook solutions

Related questions

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|