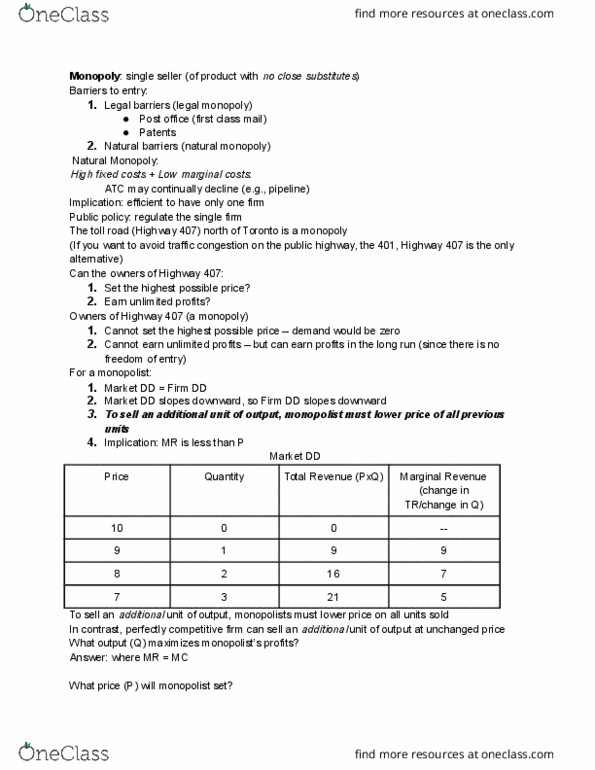

ECO101H1 Lecture 16: Lecture 16-Monopoly

Monopoly

Definition:

Single Seller (of product with no close substitutes)

Barriers to entry

(1) legal barriers (legal monopoly)

- post office (first class mail)

- patents

(2) natural barriers (natural monopoly)

Occurs when one firm can supply entire market at lower average cost than

two or more firms Ù economies of scale over the relevant range

Natural Monopoly Example: Pipeline

One firm can produce for entire market at lower cost than 2 or more firms

High fixed costs (pipeline) plus low marginal cost (maintaining pipeline)

=> ATC falls over relevant range

Natural Monopoly

1. Economies of scale (declining ATC) = barrier to entry

2. If monopolist (say, gas pipeline) is making economic profits, will new firm enter?

NO.

2nd firm would have higher ATC (as would 1st firm) if market is shared

**Past Tests 2 posted on site

www.notesolution.com

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

Single seller (of product with no close substitutes) Barriers to entry (1) legal barriers (legal monopoly) Occurs when one firm can supply entire market at lower average cost than two or more firms economies of scale over the relevant range. One firm can produce for entire market at lower cost than 2 or more firms. High fixed costs (pipeline) plus low marginal cost (maintaining pipeline) 2nd firm would have higher atc (as would 1st firm) if market is shared. **past tests 2 posted on site www. notesolution. com (mr) < price (p) very important. Because the market demand curve slopes downward, a monopolist must lower price to sell more output (p x q) At q = 2, mr = 7 < p = 8. At q = 3, mr = 3 < p = 6 if price is 6, demand is 4. If person wants to increase output, must lower price.