ACTG 2010 Study Guide - Final Guide: Cash Flow Statement, Accounts Receivable, Accounts Payable

Document Summary

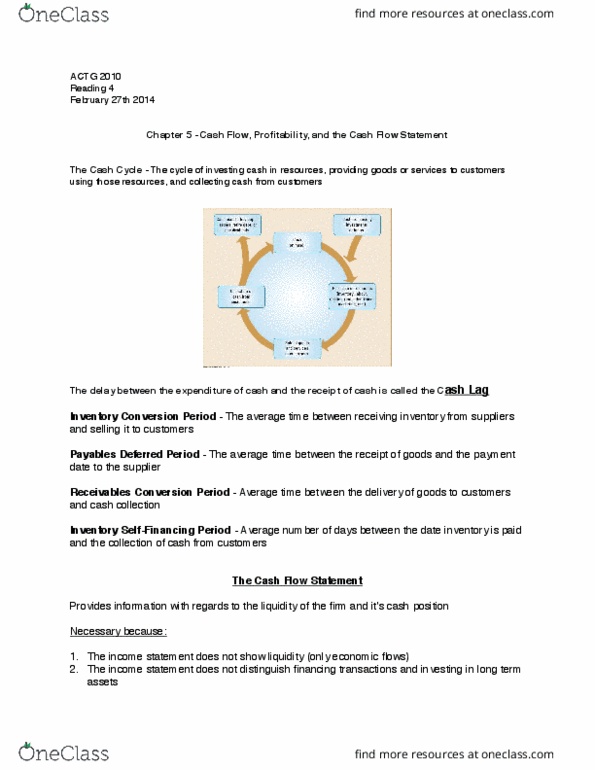

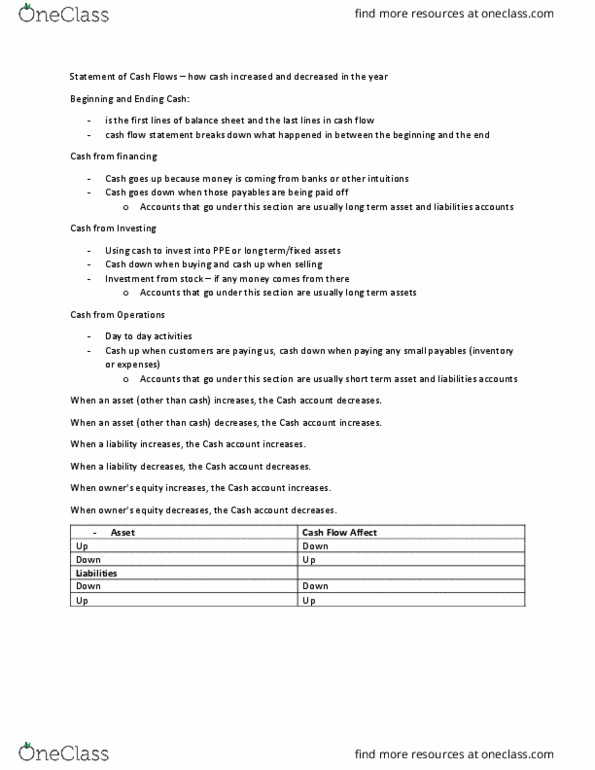

Chapter 5 cash flow, profitability, and the. There is always a lag b/w expenditure and receipt of cash = cash lag: 4 cash lag calculation (all. Keep in mind that growing businesses are always different may have a good record b/c the business just started. Cash and cash equivalents = cash on hand and in banks, short term liquid investments (gics, commercial paper, short term deposits, treasury bills, money market funds) also lines of credits. Proceeds from sale of securities like stocks and bonds. Capitalized and cash spent on pre-opening costs, oil exploration costs. For direct method, measure strictly only cash received and cash paid: *careful: cash paid/received could be still influenced by increase/decrease in accounts, eg) if revenue was 2000, but increase in accounts receivable was. 200, means only 1800 cash was collected from customer. For indirect method: *always put net income first, then depreciation then worry about current assets/current liabilities.