MGAB01H3 Chapter : Merchandising Operations

27 Oct 2010

School

Department

Course

Professor

16

MGAB01H3 Full Course Notes

Verified Note

16 documents

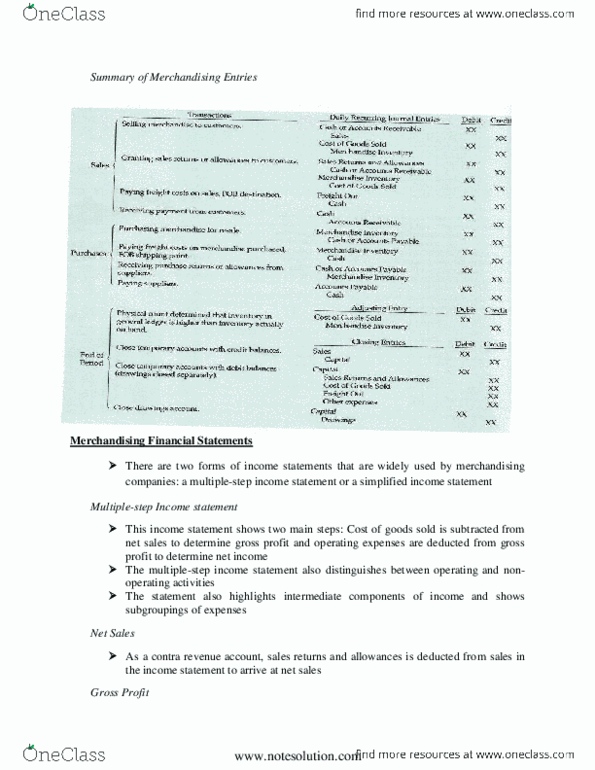

Document Summary

The primary source of revenues is the sale of merchandise. These revenues are referred to as sales revenue, or simply sales. Expenses for a merchandising company are divided into two categories: cost of goods sold, and operating expenses. The cost of goods sold is the total cost of merchandise sold during the period. This expense is directly related to the revenue earned from the sale of goods. Sales revenue less cost of goods sold is called gross profit. Operating expenses are expenses that are incurred in the process of earning sales revenue. Gross profit operating expenses = net income (or net loss) The operating cycle of a merchandising company is the average time from the purchase of merchandise inventory and its eventual sale. There are two main inventory systems: perpetual inventory system or a periodic inventory system. In a perpetual inventory system, detailed records of each inventory purchase and sale are maintained.