ACC 406 Lecture Notes - Lecture 4: Total Absorption Costing, Pro Rata, Bid Price

18 Apr 2017

School

Department

Course

Professor

Document Summary

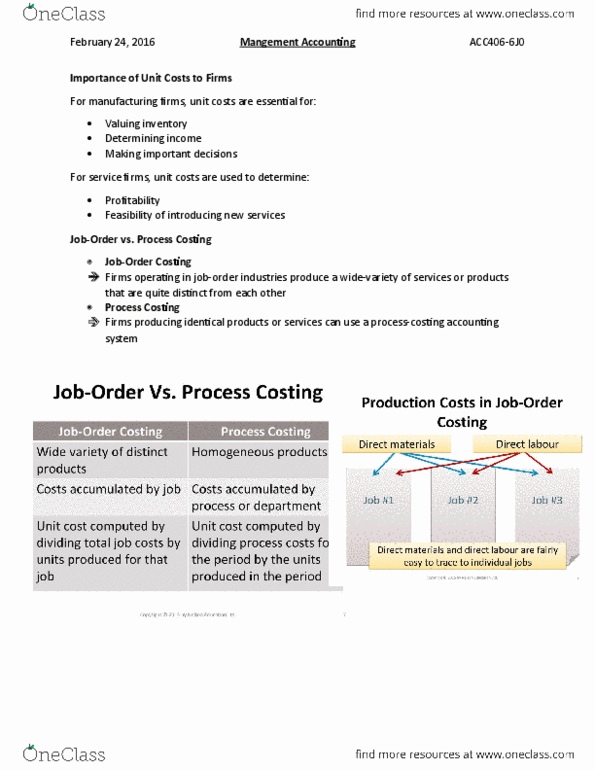

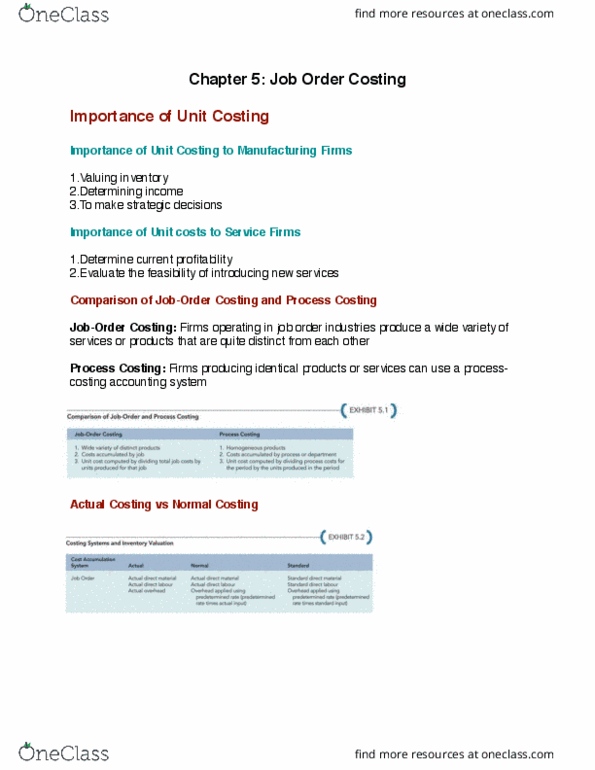

Homework: p5-29, p5-30: a set of accounting procedures by using accounts to accumulate cost in and distribute cost out. Product costing system: a costing system in which the product itself is the cost object. Job order costing system: a major example of product costing system. Fixed overhead is included/applied to/absorbed by product units i. e. cost of goods manufactured = Direct material + direct labour + total overhead the total overhead means both total variable overhead and total fixed overhead. When company excludes fixed overhead cost from product costs, and expensed in the accounting period cost of good manufactured = dm +dl. Need overhead rate= overhead cost / activity volume. Actual overhead rate= overhead cost / activity volume. Most people feel this method is better because it is more objective, reliable, based on real information used by financial accounting. Predetermined means it is estimated and not actual. Estimate that the expected overhead cost is ,200.