COMM 121 Chapter 6: Chapter 6A

9 Oct 2013

School

Department

Course

Professor

Document Summary

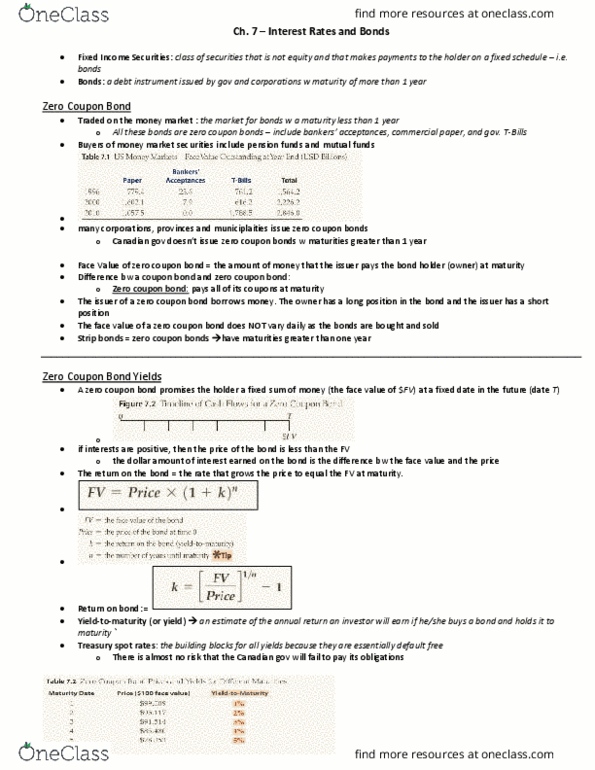

Chapter 6a: the term structure of interest rates. So far we have assumed that interest rates are constant over the all future periods: they actually vary over time because inflation rates differ over time. The spot rate is the interest rate over one period of the investment. If we want to calculate a single rate for the bond: ( ) solve for r: pv(known) = The term structure describes the relationship of the spot rate with different maturities. We will begin by defining the term forward rate and relate it to future interest rates. If an individual can earn a 10% spot rate over two years, it is equivalent if he were to earn. 8% in the first year and 12. 04% (( ) ) during the second year: this hypothetical rate over the second year is the forward rate. So: (1+r2)2 = (1+r1) x (1+f2) f2 = ( Estimating the price of a bond at a future rate.