ACT370H1 Lecture Notes - Delta Neutral, Log-Normal Distribution, Interest Rate

Document Summary

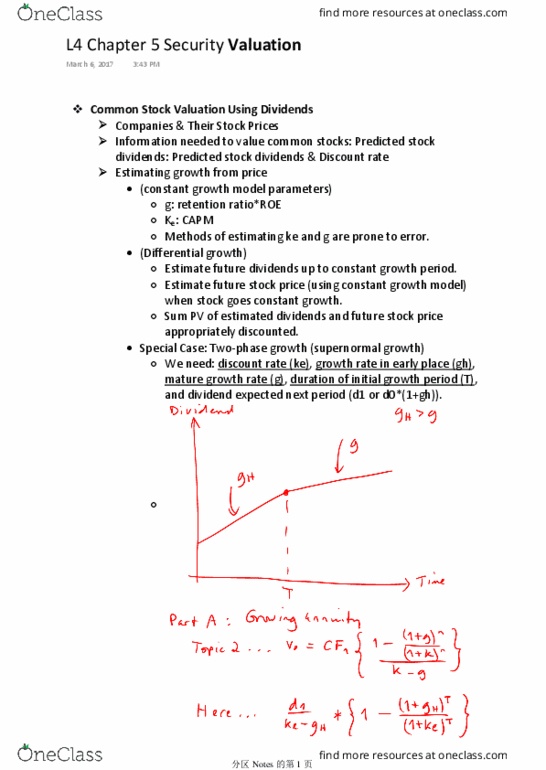

Leverage inherently risky small amount of cash -> large effect. Theoretical stock price = 1/ , assuming constant dividends (rate ) forever. All of our work here is based on predictable dividends and mostly on regular payments. Iv = intrinsic value (s-k or k-s) as if we could exercise the option right now (for european, pretend you can exercise now) Tv = time value comes from the belief/hope that there will be favourable conditions by exercise time. Tv decays to zero as we approach expiration date. Partial derivatives showing how an investment price responds to observable variables. In this course, we focus on singles (for options) However, hull uses portfolio notation ( ) but discusses options. Portfolio could consist of just one investment. (theta) = / t (calendar time) or - / t (remaining time) Q: if stock price goes up, will call price: go up, go down c)