ECON101 Lecture Notes - Marginal Revenue, Marginal Cost, Opportunity Cost

73 views24 pages

8 Apr 2014

School

Department

Course

Professor

79

ECON101 Full Course Notes

Verified Note

79 documents

Document Summary

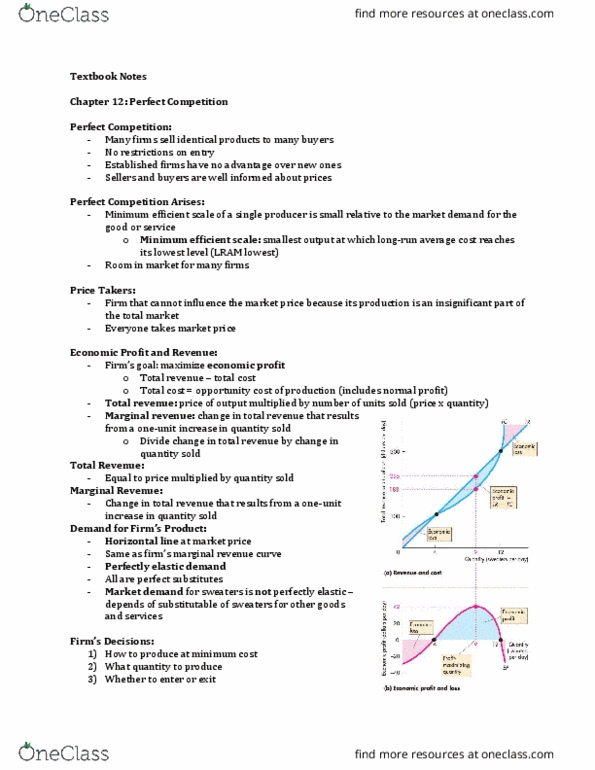

No single firm can influence the price it must take the equilibrium market price. Total cost is the opportunity cost of production, which includes normal profit. Because in perfect competition the price remains the same as the quantity sold changes, marginal revenue equals price. The firm maximizes its economic profit when it produces 9 sweaters a day. The firm can use marginal analysis to determine the profit maximizing output. Because marginal revenue is constant and marginal cost eventually increases as output increases, profit is maximized by producing the output at which marginal revenue, mr, equals marginal cost, mc. Figure 12. 3 shows the marginal analysis that determines the profit maximizing output. If mr = mc, economic profit decreases if output changes in either direction, so economic profit is maximized. If the firm decides to stay in the market, it must decide whether to produce something or to shut down temporarily.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers