BUSI 2400 Study Guide - Quiz Guide: Tax Credit, Life Annuity, Cape Breton University

24 Jan 2016

School

Department

Course

Professor

Document Summary

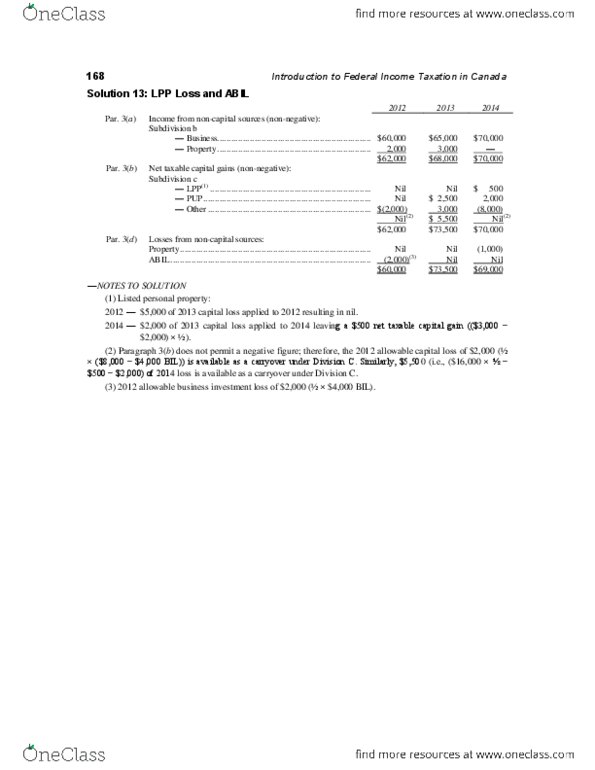

Net taxable capital gains on listed personal property (lpp) Sme inc. shares (62,000 x = 31,000) [exception 1a available because the price paid was lower than the fmv at grant date](price paid > fmv grant date ) [exception 1b not available on disposition because deduction under 110(1)(d) even if ccpc and shares keep for 2 years] Net capital loss (other than lpp) carry-over. Universal child care benefit (uccb) (#12) (sia income) Note e - capital gains (cg) / capital losses (cl) Ms: exemption 59,000 x (2 + 1) / 3 (2 years = 19x9 + 20x0) (full exemption for principal residence) Capital gains (cg) and taxable capital gains (tcg) Capital losses (cl) and allowable capital losses (acl) Adjusted cost base (acb) (no loss on pup) Cl and allowable capital losses (acl) (excluding abil) Bil and allowable business investment losses (abil) (note i) Cl and allowable capital losses (acl) (including abil)