COMM 305- Midterm Exam Guide - Comprehensive Notes for the exam ( 52 pages long!)

4 Oct 2017

School

Department

Course

Professor

Document Summary

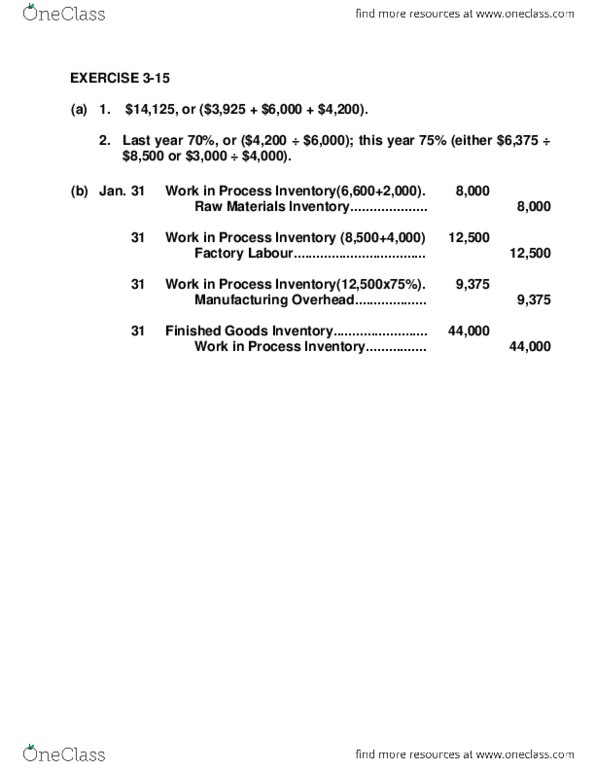

Costs are assigned to each job or batch. A job may be for a specific order or inventory. A key feature: each job or batch has its own distinguishing characteristics. The objective: to calculate the cost per job. Measures costs for each job completed not for the set time periods. Used when a large volume of similar products are manufactured. Cost are accumulated for a specific time period. Costs are assigned to departments or processes for a set period of time. *** be able to understand the difference between the two and be able to use examples !! There"s two (cid:373)ajor steps i(cid:374) flows of costs: accumulate the manufacturing costs incurred. Manufacturing overhead: assign the accumulated costs to the work done. Consists of: gross earnings of factory workers, employer payroll taxes on such earnings, fringe benefits incurred by the employer. May be recognized daily: for example, machinery repairs, indirect materials, and indirect labour.