FIN 300 Study Guide - Payback Period, Cash Flow, Net Present Value

5 May 2011

School

Department

Course

Professor

Document Summary

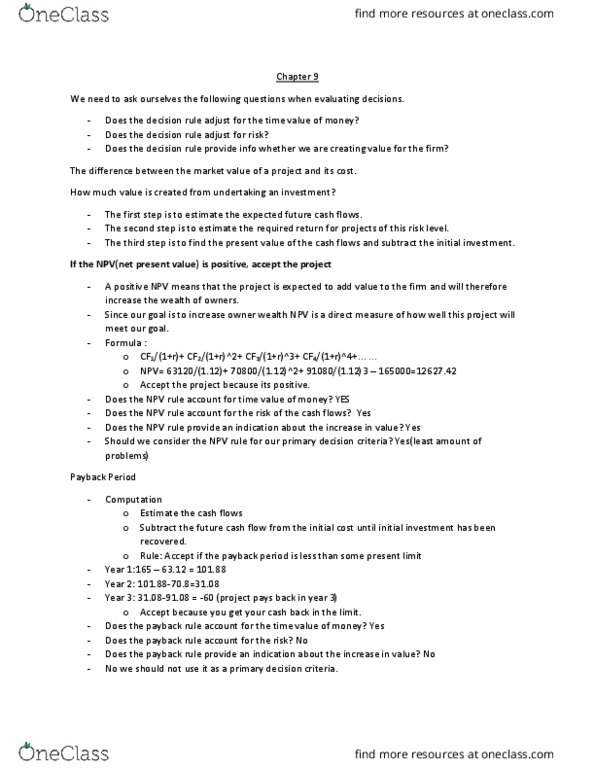

Answers to concepts review and critical thinking questions. A payback period less than the project"s life means that the npv is positive for a zero discount rate, but nothing more definitive can be said. The discounted payback includes the effect of the relevant discount rate. If a project"s discounted payback period is less than the project"s life, it must be the case that npv is positive. If a project has a positive npv for a certain discount rate, then it will also have a positive npv for a zero discount rate; thus, the payback period must be less than the project life. Since discounted payback is calculated at the same discount rate as is npv, if npv is positive, the discounted payback period must be less than the project"s life. If npv is positive, then the present value of future cash inflows is greater than the initial investment cost; thus pi must be greater than 1.