FIN 502 Study Guide - Final Guide: Potato Virus X, Debt Service Ratio, Cash Flow

22 Apr 2014

School

Department

Course

Professor

Document Summary

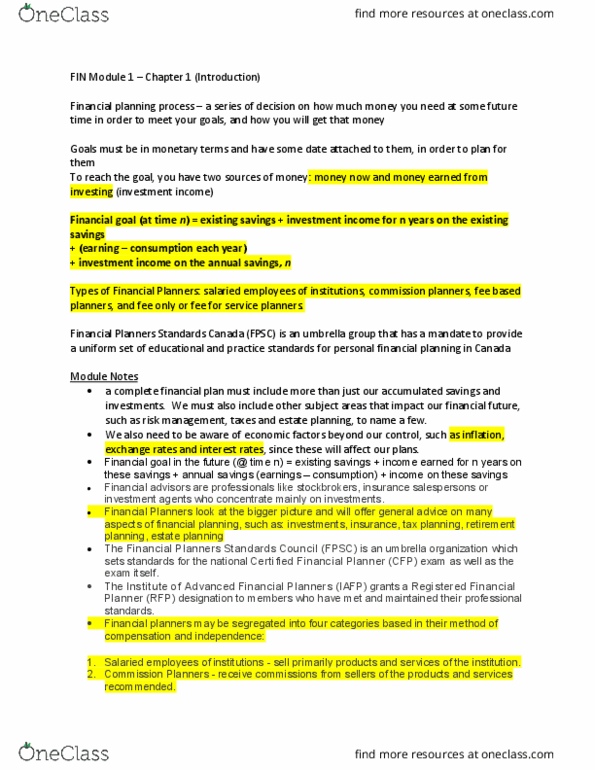

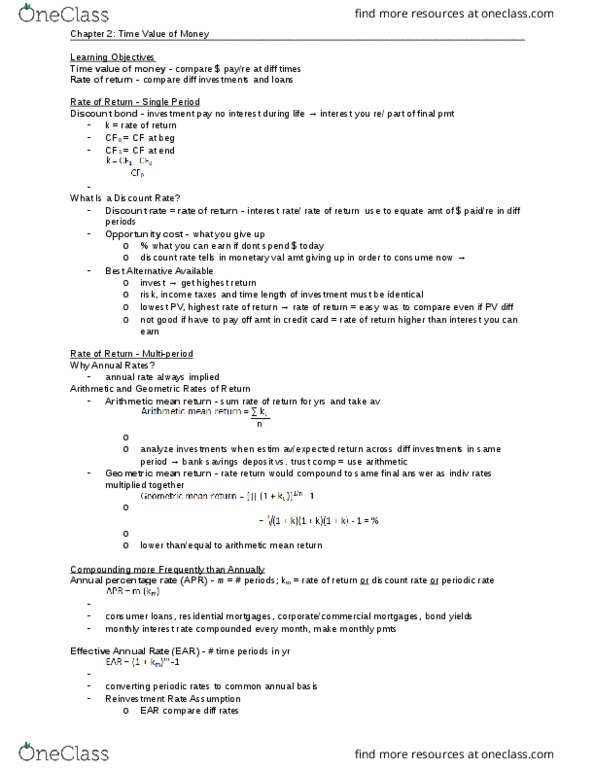

Chapter 1: intro: financial planners (four categories): salaried employees of institutions, commission planners, fee-based planners, fee-only (for service) financial planners. Chapter 2: time value of money: kt. = return in period t reinvestment rate assumption: concerns at what rate the periodic rates are reinvested ear assumes that the periodic payments are reinvested at the same rate as the original loan . Rate of return: multi period, arithmetic mean return = n kt t =1 n (e. x. Annual percentage return (apr) = m x km , m= number of periods, km= rate of return. Future and present value: single period, fv =pv (1+k ) F&p value: multi-period (compounded), fv =pv (1+k )t. Pv = fv (1+k)t g=constant growth rate, x= first payment or cash flow of cga. Nominal rate: 1+knom=(1+kr)(1+i) knom=(1+kr) (1+i) 1 or knom=nominalrate ,kr=real rate ,i=inflationrate. Rate of return: mp, geometric mean return= (1+kt) n. or use 1. 4822 as fv, -1 as pv, 4 as n, cpt i/y.