BUS 320 Study Guide - Financial Statement Analysis, Reserve Requirement, Current Liability

31 May 2011

School

Department

Course

Professor

Document Summary

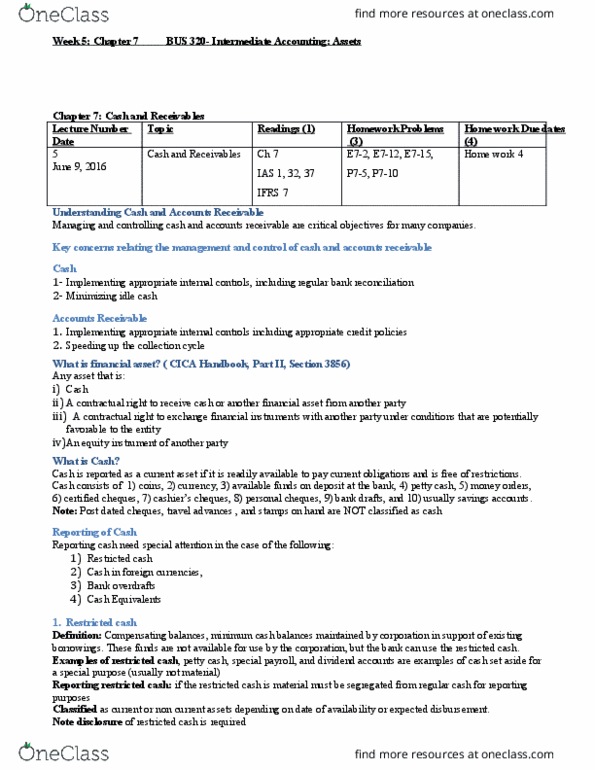

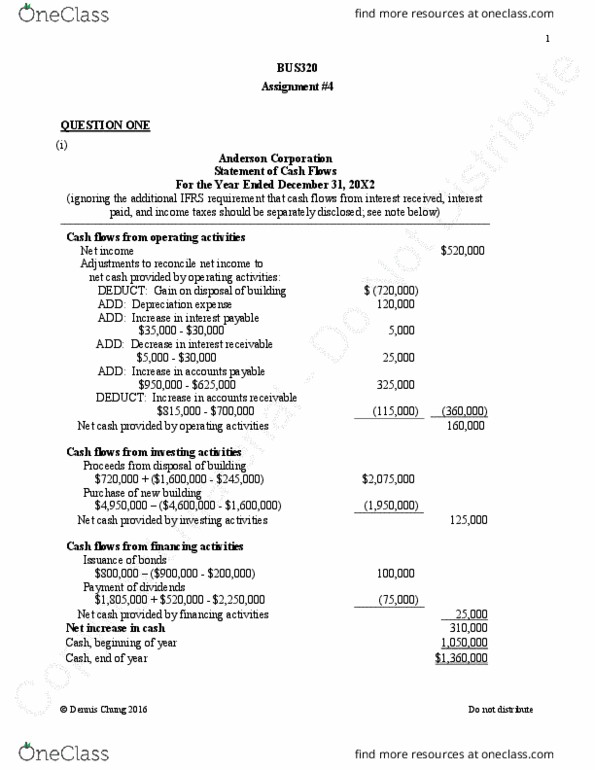

3. 1 cash flow and financial statement: a closer look. Cash is generated by selling a product, an asset, or a security. Selling a security involves either borrowing or selling an equity interest (i. e. shares of stock) in the firm. Uses of cash: a firm"s activity in which cash is spent. An increase in a left-hand side (asset) account or a decrease in a left-hand side (liability or equity) account is a use of cash. Likewise, a decrease in an asset account or an increase in a liability (or equity) account is a source of cash. The net addition to cash is just the difference between sources and uses. Statement of cash flow is a firm"s financial statement that summarizes its sources and uses of cash over a specific period. We are trying to group all changes into three categories: operating activities, financing activities and investment activities.