FIN301 Final: Final Finance 301 Cheat Sheet TU.docx

Document Summary

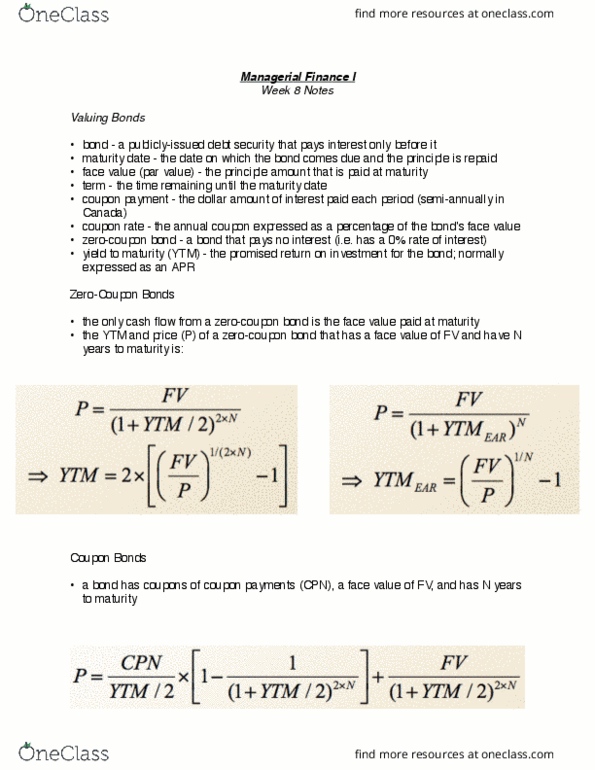

N(d1)- e- rt k n(d2) ] = rf + b i e rm[ Longer maturity/lower coupon rate/less frequent coupons, high duration. Duration underestimates gains/overestimates loss if r changes by 1%, bond price changes by %duration. Effectiverate=(1+ear) if compounding pd= paymnt freq , asap. 1 m 1 zero coupon bond= duration/maturity (6 yr 0 coupon bond has d=6) Usually quoted apr semi annual rate need ear monthly. Po= c (1+r)t]+ f r [1 1 (1+r)t. To discount it you either use nominal pv and nominal rate to discount or inflation pv over the real rate. Po= d (1+r)t = d r (cid:230) (cid:231) (cid:246) (cid:230) (cid:231) (cid:246) b b b. But if given a finite time use an annuity: Po= (1+g)t r g[1 (1+r)t] r [1 1 (1+r)t] = 1 r means nogrowth g=b roe if r > roe , shareholders are . Front loaded cash flows have higher irr but less npv than back loaded else, value destroying.