MGEC71H3 Study Guide - Final Guide: Business Cycle, Accrued Interest, Commercial Paper

26 May 2012

School

Department

Course

Professor

Document Summary

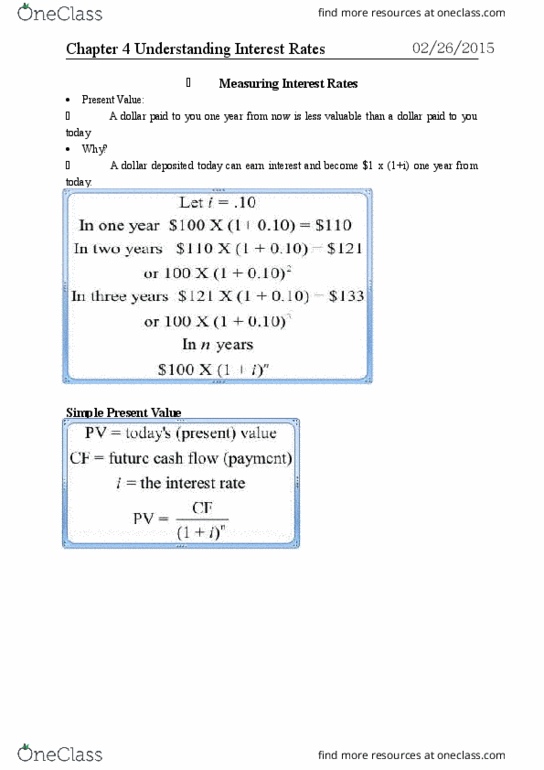

Present-value- based on the notion that a dollar paid one year from now is less valuable to you than a dollar paid today. Generally we can generalize the simple loan with this equation: There are basically four basic types of credit market instruments: a simple loan, already outlined in the equation above, a fixed-payment loan aka. 1: in general, for a one year discount bond, the yield to maturity can be written as. Assumes re-investing in another t-bill with the same term to maturity (until get 1 year) with the same. As with a coupon bond, the ytm is negatively related to the current bond price. As the yield to maturity falls, the price of the bond rises: the reasoning behind this is because with a higher interest rate, the payments are worth less, if i > c then p < f. If i < c then p > f.