MGAB02H3 Study Guide - Final Guide: Asset Turnover, Profit Margin, Issued Shares

Document Summary

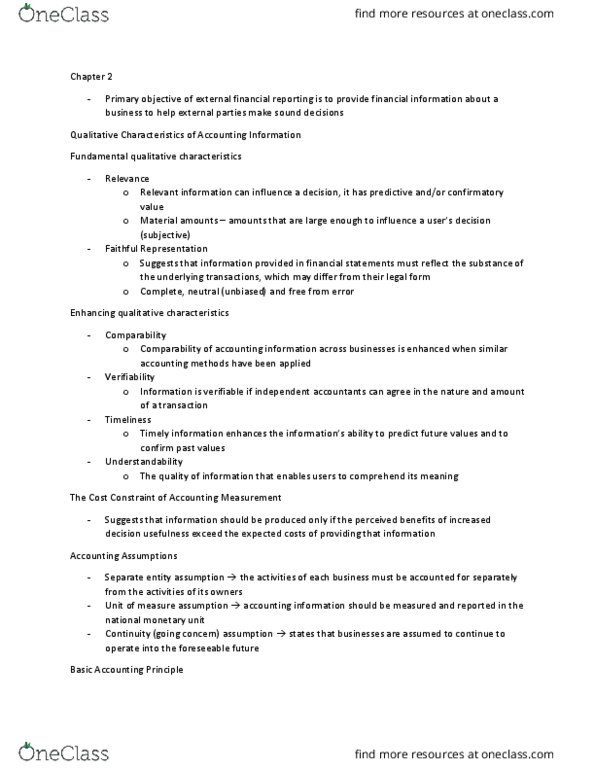

Primary objective of external financial reporting- to provide economic information to external users for decision making. Secondary qualitative characteristics: comparability: across business, consistency: over time, understand ability. Separate entity- transactions of the business entity are separate from transactions of owners. Going concern/ continuity- the entity is expected to continue its operations in the foreseeable future. Justifies the use of cost principle (benefit is still there even though the value is going down) Stable dollar/ unit of measure- only include items that can be measured in the national monetary unit (%). Purchasing power of the unit of measure does not change over time. (if you cannot measure it, you cannot record; must be verifiable) Time period- the long life of a company can be reported over a series of short time periods necessary to prepare annual f/s. Historical cost- the cash equivalent cost given up is the basis of initial recording of financial statement elements.