Pricing

Log in

Sign up

Home

Homework Help

Study Guides

Class Notes

Textbook Notes

Textbook Solutions

Booster Classes

Blog

Home

Study Guides

420,000

CA

160,000

RSM332H1 Study Guide - Final Guide: Implied Volatility, Call Option, Capital Asset Pricing Model

50

views

1

pages

lemonbadger175

10 Oct 2019

School

UTSG

Department

Rotman Commerce

Course

RSM332H1

Professor

Kevin Wang

Like

For unlimited access to Study Guides, a

Grade+

subscription is required.

Get access

Grade+

$40

USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Continue

Related Documents

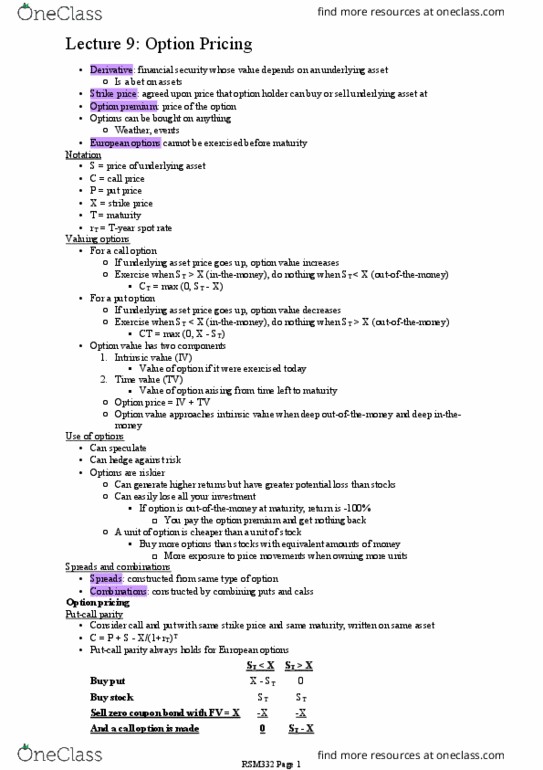

RSM332H1 Lecture Notes - Lecture 9: Strike Price, Call Option, Spot Contract

lilacoyster158

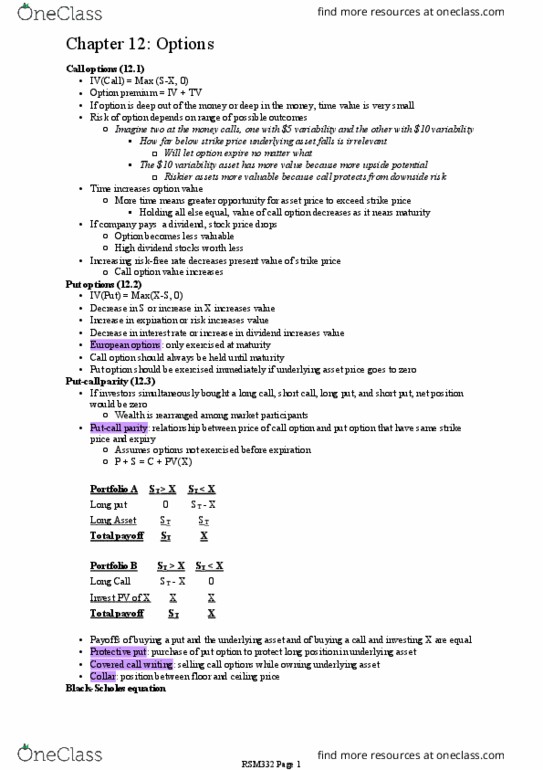

RSM332H1 Chapter Notes - Chapter 12: Call Option, Downside Risk, Put Option

lilacoyster158

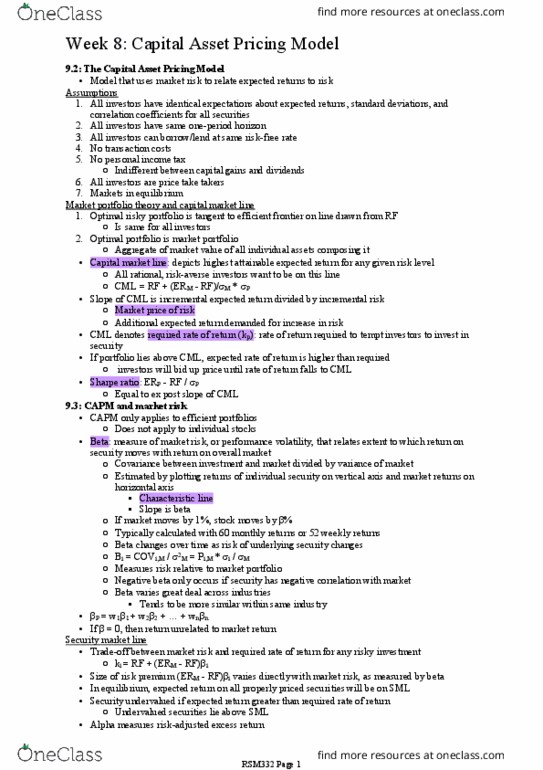

RSM332H1 Chapter Notes - Chapter 9: Risk Premium, Capital Asset Pricing Model, Market Portfolio

lilacoyster158