Business Administration 2257 Study Guide - Final Guide: Fixed Asset, Chinese Professional Baseball League, Cash Out

30 Apr 2018

School

Department

Professor

1. Understand Organization

Industry analysis

Consumer Analysis

Competitive Analysis

Corporate Capabilities

2.Financial Size-Up

Statement of CA flow

Ratio Analysis

Contrib Analysis

Segment Reporting

- if not enough info, = 0 (ex: advances,

indebts, CPBL = 0 and BL is same as last

year); Common Stock= same if no new info

given

- under LT liability, differential loan = PLUG

** IF BL (plug) needed = reminder @ next

end of year; assume loan needed= total $ for

entire expansion *could be plug on equity if

too much debt previously taken

Alternative Financing: short term options

(take line of credit to cover short term uses,

sell fixed assets, change credit terms to free

up cash) DECIDE!

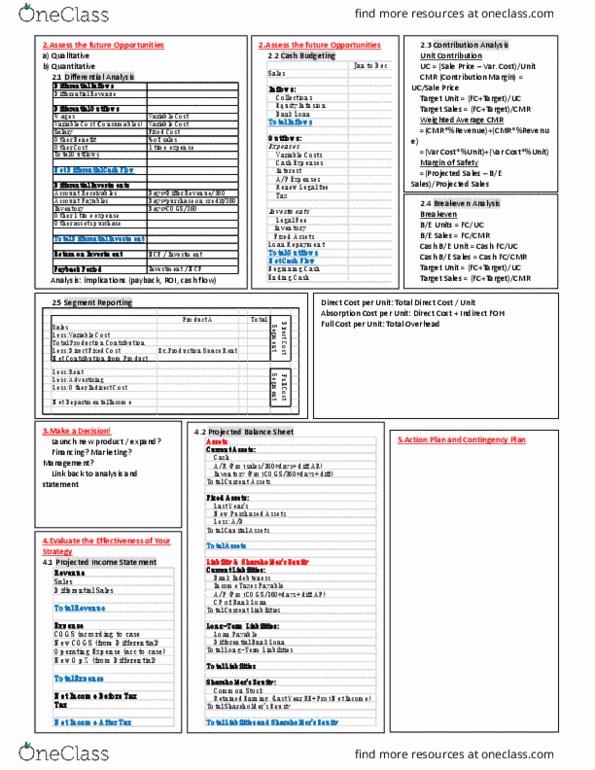

Cash Budgeting: For Months / Year of ___

Months/Year Total

Inflows

Sales, CA, Receivables, loan, etc.

Total Cash In

Outflows

Op. exp (inventory, rent, telephone, insurance, supplies, sal

commission, office equip, interest, drawings

Total Cash Out

Surplus or Deficit (cash in minus cash out)

Opening cash Balance (last years)

Closing Cash Balance (projected)

measures solvency + ability to meet cash demands as they fall

due, look for hint “break down from month to month” “short on

cash” make conclusion: need line of credit to keep aflow = loan

= needs to be built into projected balance sheet + might be PLUG

if every month has (+) CA = GOOD, (-) CA will go bankrupt

and company can survive if unprofitable BUT not if NO CASH

Predicting new product lines -- segmenting

3 costs: DIRECT = material, labor, selling exp (VC)

ABSORPTION = direct + fixed product (changes per unit w volume)

FULL = absorption + other expenses = accounts for total op of business

**FC related to Absorp + business OP (Full) must be allocated through

segments FC allocation rate = Total FC / Total proxy (DL

** where proxy is an item spread evenly throughout process overhead

per unit = Fixed cost alloc. Rate X Total Proxy per unit

Interpretation: Direct Costs (min price form could charge w/o loss)

Absorption/Full cost = breakeven analysis (FC / UC) = compares

product/plant efficiencies, profitability of each product, which to promote?

3.Assess Future Opportunities

1.Qualitative

2.Quantitative:

diff analysis **BOLD = must do

contrib analysis

breakeven analysis

segment reporting

CA budgeting

4.MAKE DECISION

Then…A)Projected Statement

SOE (income w Rev + Exp + NIAT)

SFP (balance sheet: A = SE + L)

B) Action + contingency plan

CA Flow Statement

WHY? business w/o cash CANNOT survive (insufficient

$ to pay debts) BUT company unprofitable CAN

are we making smart mgmt. decisions? where $ from?

Operation: Income, Add back NON CA (-gain/+loss, dep),

changes in op (refer to purple box of use / source) includes

a/r, inv, rent, prepaid, current liabilities, accruals, A/P

**ADD SOURCES, SUBTRACT USES

= NET CASH FLOW FROM OPERATIONS

Financing: includes bank loan, mortgage pay, bonds, CP,

stock, dividend (retained earning formula to find dividends)

= NET CASH FLOW FROM FINANCING

Investment: investments/disinvestment (withdrawing invest)

look @ noncurrent assets + record changes (use + source)

net fixed asset formula ( - losses, + gains)

THEN…add all three, and add to beg CA to get END CASH

CA Flow Analysis

Is Net Cash Flow from Op +? must be

engine of business

driven by NI? GOOD if it is!

where are major sources / uses

look at A/P, INV, and A/R (calculate days

+ ratios)

A/P = $ u owe ppl, too high = not good

relationship w suppliers, can A/P be extended

further?

A/R = $ owed to us, use of CA from this

means ppl owe us more (+ could be selling

more so amount ppl paying us more OR – if

ppl take longer to pay us = not good, can we

make them pay us sooner, change credit

terms?)

days of A/R consistent = selling more

BUT if it goes up a lot then ppl taking longer

to pay us

Inv = decreased means selling less b/c

shortage on inv OR better w Inv =not keeping

too much on hand days of INV

Matching

short term sources to short term uses (LT

Bank loan for LT fixed asset = good but if for

A/R, A/P, INV = BAD

Additional Financing?

Debt OR equity (debt preferred b/c lose

ownership w equity but debt has interest)

are there large investments, are we

growing, are assets used effectively (ratios)?,

company expanding operations/ when to get

line of credit / LT loan, Internal Financing?

(A/P, A/R, INV)

Differential Analysis remember:

subtract lost sales of old product,

and add COGS saves of investing in

new product, compare ROI against

hurdle rate –probably interest from

bank, perform sensitivity analysis

(consider variables that are subject to

significant uncertainty)

if business operates for only 120

days, use this instead of 360

SUNK COSTS like research +

development (already paid for)

should not be included

MAKE DECISION!!

based on goals + objectives

then…projected statements (only

low)

**decision: what to do? How to

finance? Debt or equity?

Requirements met? Fit with

analysis? Highlight main risks/

mitigations? Qual vs quan?

Penis☺

Differential Analysis: must be future, affect cash,

different b/w alternatives, recurring (decides: make in

house vs buy, lower / raise prices? Expand vs status quo?

before this, pro vs. con qualitative chart of alternative

then quan: label as inflow, outflow, invest and total

them and do ROI (net ca flow/total diff invest), payback

(total diff invest/net ca flow) **does not include

depreciation b/c non cash **no finance costs

investments: one time expenditures, working capital

(include unless negligible)

Diff Inv = Diff COGS ($) / 360 Days X Days Inventory

Diff A/R = Diff Credit Sales / 360 X Days AR

Diff AP = Diff purchases or COGS X Days AP

If footnote says _ only related to _ then replace diff #

AR = (+) = increasing b/c something (ex: sales)

increasing = ppl taking longer to pay = decrease in CA =

USE of cash

AP =(-)= getting cash=increase in cash = SOURCE

*use suggested days of WC = if new customers acquired

*use current days of WC = if same customers being used

Marketing:

PUSH:

business TO

customers, motivate

retailer to buy product on

shelves & hope they buy

**distribution channels

IMP

PULL:

market to customers &

make THEM demand

product. b/c customers

want = retailers obligated

to give shelf space & ask

us to supply product

** end user IMP

Management:

Environ – trends in

industry /economy?

Company -- $ for

financing? How are we

doing?

Customer – target market,

where to buy + why us?

Competitors – who are

they?

Plan:

4 P’s (product, price,

promotion (ads),

placement (distribution)

Goals:

Increase customer

retention, inc. willingness

to pay, inc # customers

Projected Statements

ONLY LOW / status quo

SOE (IS): look @

original one + follow

format, calc sales change

(same %? Multiply by

new sales), add

differential sales,

depreciation= old + new

deprec = (total fixed A /

UL) + (new Assets/ UL)

for expenses: account for

changes (ex: projected

sales X % of salaries

increase)

SFP: (balance sheet):

look @ original and

follow format, add case

facts (enter same dollar

items unless told

otherwise)

-calculate RE = proj. NI +

last yr RE – div/drawings

-Acc Dep. = old + new

(from IS)

- projected AR, AP, INV:

A/R = diff AR + normal

AR = proj. sales/360 X

current days AR

AP = (COGS from

IS/360) X current days

AP – diff AP (saving $)

OR + diff AP (loss)

Inv= proj. purchases or

COGS X days inv / 360

find more resources at oneclass.com

find more resources at oneclass.com