Business Administration 4437Q/R/S/T Study Guide - Final Guide: Income Splitting, Employee Stock Option, Tax Bracket

3 Nov 2011

School

Department

Professor

Document Summary

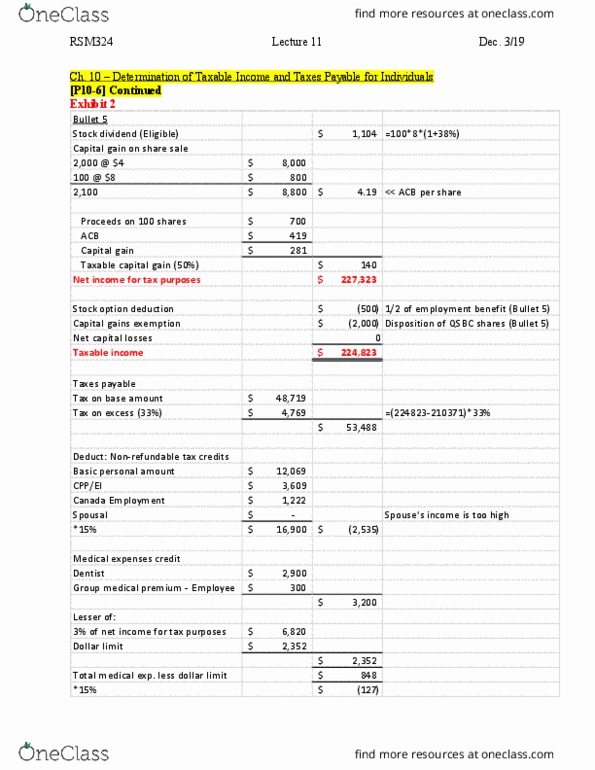

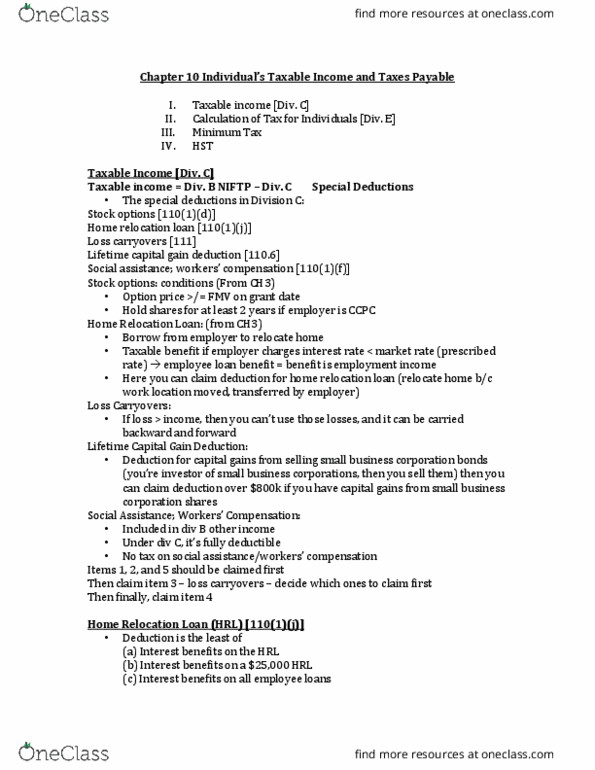

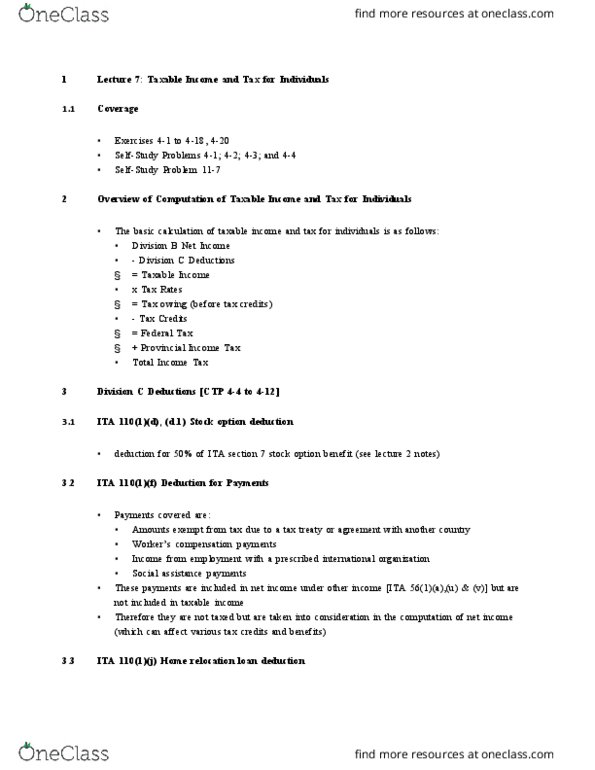

Bus4437q/r - income tax planning - final exam notes: determining taxes payable for an individual. Net taxable capital gains (1/2 of capital gain taxable) Loss carryovers, employee stock options, home relocation loan, ad capital gains exemption (,000 or ,000 taxable gain on cumulative life- time on disposition of qsbc shares and family farming and fishing businesses) On excess at 29% = (,000 - ,021) = ,979 x 29% = ,314. Federal tax before credits = ,880 + ,314 = ,194. Tax credits: two flavours federal tax credits and provincial tax. Most tax credits reduce basic federal tax and are non-refundable in nature. Act permits some credit transfers and carry forwards. General rule: federal non-refundable tax credits are calculated by multiplying a base by 15 per cent. Most common tax credits see appendix a (casebook) Basic federal tax: capital property vs. business income.