BU227 Study Guide - Final Guide: Asset, Contingent Liability, Current Liability

Document Summary

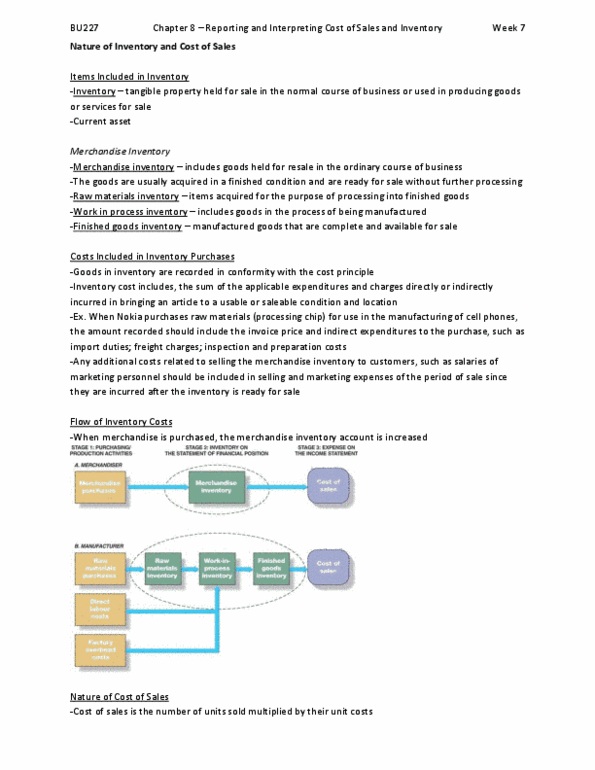

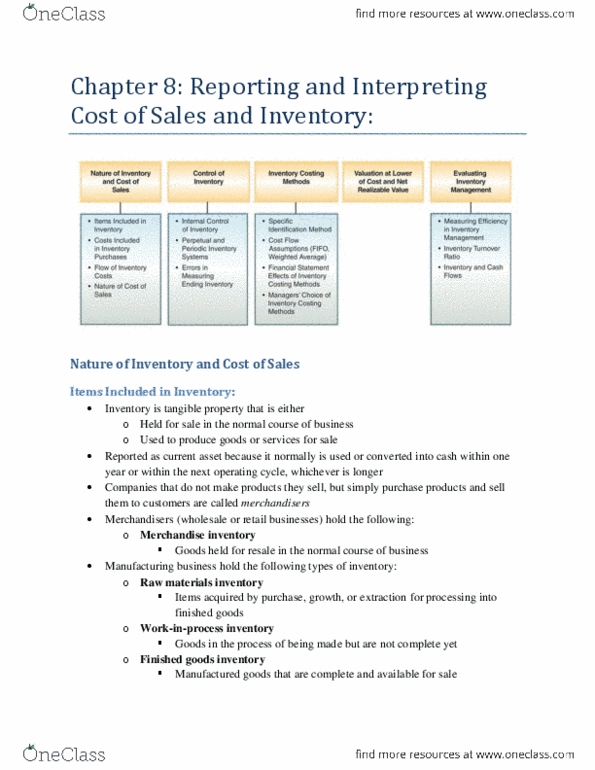

Chapter 8: reporting & interpreting cost of sales & inventory periodic -> purchases, carries over to end of period perpetual -> inventory, recorded at every sale. Speci c identi cation: speci c cost of item sold is added to cost of sales. Fifo method: cost of most recent purchases are in ending inventory. Begin adding [# of units] from the most recent date, until you have reached the # of units of ending inventory. Whatever is left over from the least recent purchase, multiply that by $/unit and add to what beginning inventory was. * fo method has been proven to have lower cost of sales, & higher ending inventory, gross inventory, income tax expense, and pro t. Cost available for sale / # of units = weighted average cost. Multiply the weighted average cost to ending inventory to get cost of that. Multiply the weighted average cost to cost of sales to get cost of that.