BU357 Study Guide - Weighted Arithmetic Mean, Fair Market Value, Property Income

Document Summary

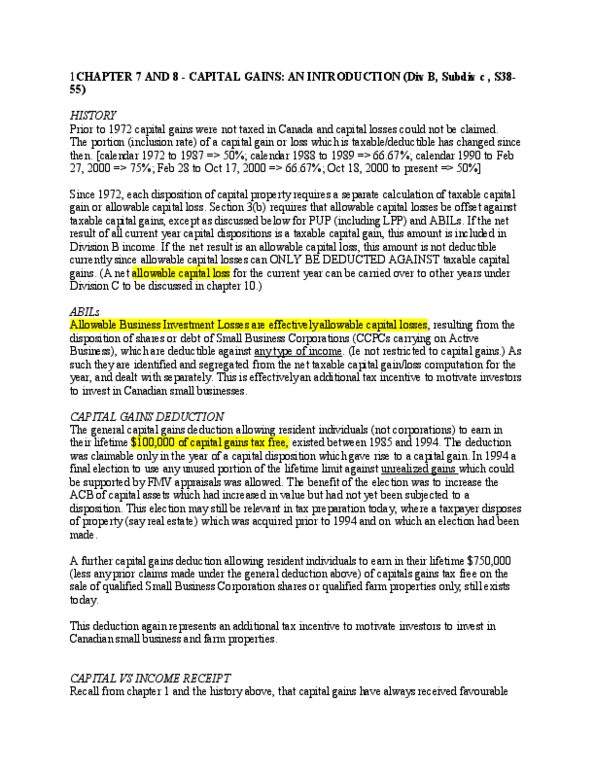

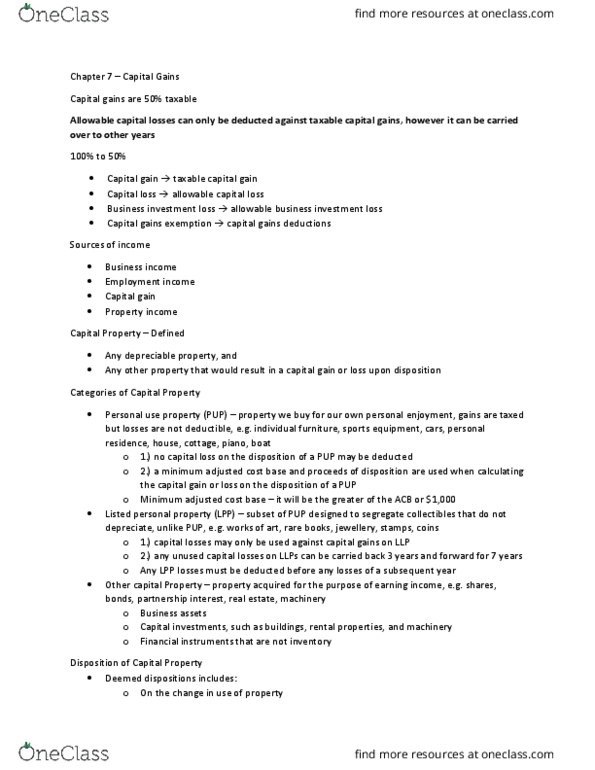

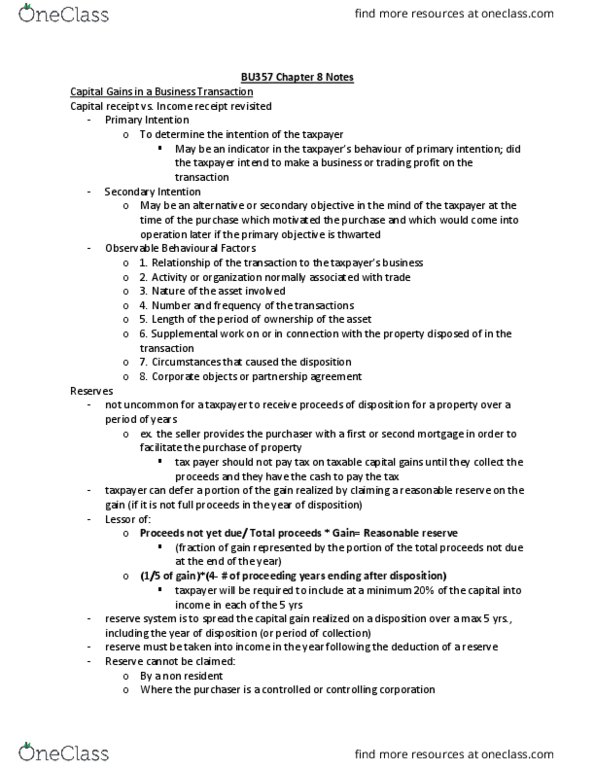

Taxable capital gain (tcg) = x capital gain/loss. Allowable capital loss (acl) is deductible only from taxable capital gains, cannot be deducted from any other source of income. The maximum reserve for any year is the lessor of: (deferred proceeds / total proceeds) x net amount or (1/5 of net amount) x (4 - # of preceding years after disposition) Problem 2 (chapter 8) anu to provide answer from notes. All gains on personal use property are taxable while losses are non-deductible (cannot reduce income). These restrictions are applied to each item of personal property. These two conditions must be satisfied in order for restriction to occur. Personal use property (pup) does have some investment value if: A print, etching, drawing, painting, or sculpture or other similar works of art. Rare folio, rare manuscript or rare book. Losses that are recognized are only deductible against gains on lpp.