BU477 Study Guide - Midterm Guide: Risk Assessment, Specific Performance, Audit Evidence

Document Summary

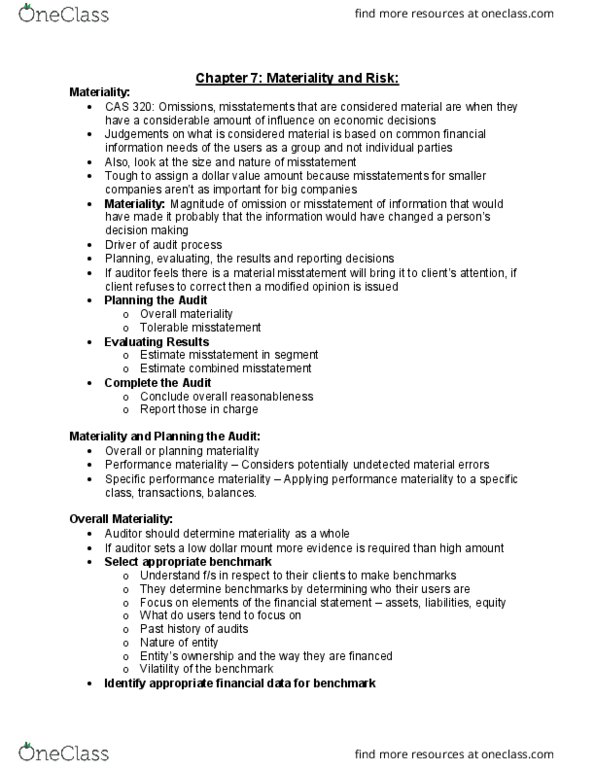

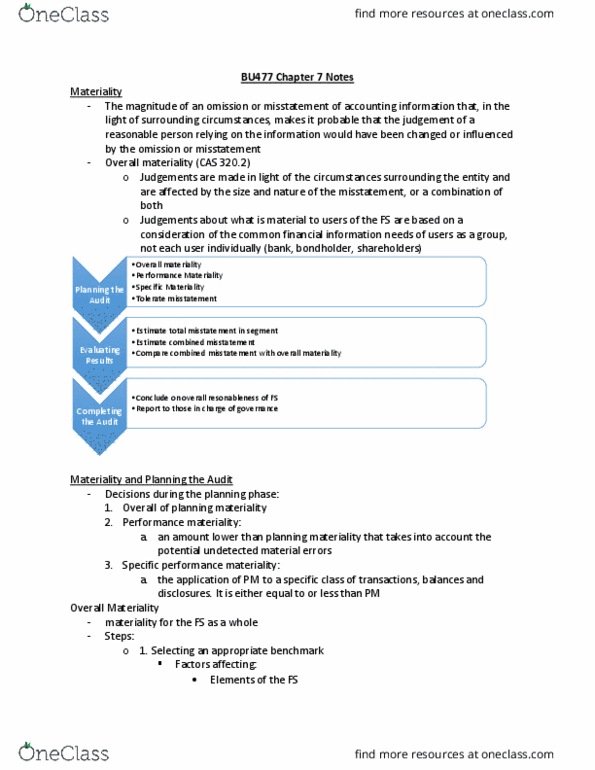

Materiality: omission or misstatement where reasonable person relying on info would have been changed or influenced by omission or misstatement. Driver of audit process planning, evaluating results, and reporting decisions. Ide(cid:374)tif(cid:455) app(cid:396)op(cid:396)iate fi(cid:374)a(cid:374)(cid:272)ial data fo(cid:396) sele(cid:272)ted (cid:271)e(cid:374)(cid:272)h(cid:373)a(cid:396)k: use p/y(cid:859)s (cid:396)esults, period to date results, and budgets for current period; adjust for significant changes and changes in industry: determine percentage to be applied to selected framework. Qualitative factors may cause auditors to adjust materiality, affecting amount of testing (e. g. effect of trends, misstatement changing loss into income, reporting requirements, misstatement that i(cid:374)(cid:272)(cid:396)eases (cid:373)g(cid:373)t. (cid:859)s (cid:272)o(cid:373)pe(cid:374)satio(cid:374)) Performance materiality: amount less than materiality used to plan audit to reduce likelihood that unexpected errors is greater than materiality: factors affecting: overall engagement risk considered high; fraud risks; history of identified misstatements; deficient control env. ; multinational: used for decisions like calculating sample size and concluding if account is materially misstated. Tolerable misstatements: performance materiality for specific sampling procedure; .