BUS-A 200 Study Guide - Final Guide: Deferred Income, Contribution Margin, Net Income

Important Formulas

• GAAP Income Statement

o Sales

o – COGS

------------

o Gross Margin (profit)

o – SG&A

------------

o Net income

• Contribution Margin Income Statement

o Sales

o – VC

-----------

o CM

o – FC

-----------

o Net income

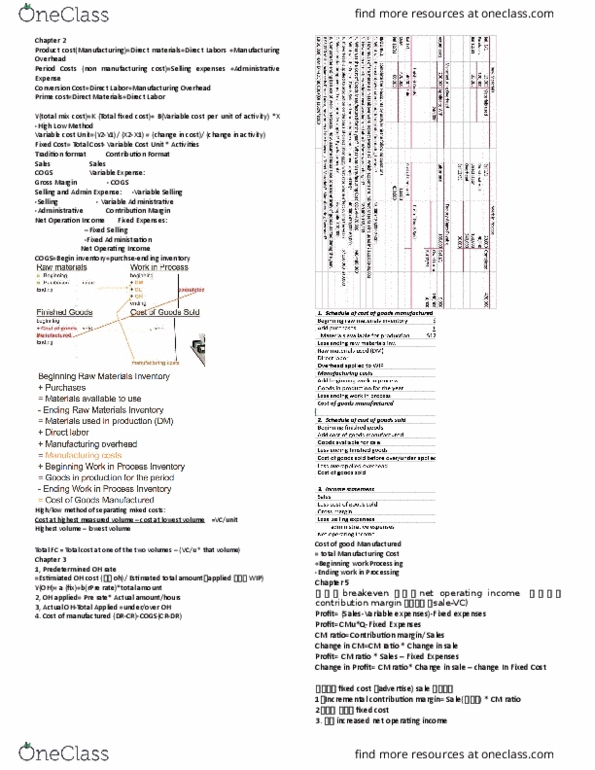

• Ending inventory = Beg inv. + purchases – COGS

• Total product cost = Materials + labor + overhead

• CM = Sales – VC

• BE = FC / (Sales – VC) or CM = # of units

• Target Volume = (Target NI + FC) / CM

• Net Income= Revenue – expenses + overhead

Chapter 1

• Double entry bookkeeping– all transactions affect the accounting equation in at least two

places

• Dividend – the transfer of some or all earned assets of a business to shareholders

• Historical cost concept – assets be reported at the amount paid for them regardless of increases

in market value

• Matching principal – pairing revenues with expenses on the income statement

• Balance sheet – A = L – OE

• Income statement – Rev – Exp = NI

• Revenue, expense, and dividend accounts are all temporary accounts

• The retained earnings from these accounts carry over to the next period

Chapter 2

• Accrual accounting requires companies to recognize revenue in the period in which the work is

done regardless of when cash is collected

• Accounts receivable the amount of cash the company expects to collect in the future

• Deferred expenses are often times called prepaid items

• Deferred revenue is a liability called unearned revenue

find more resources at oneclass.com

find more resources at oneclass.com

Chapter 3

• Service business

o NI = Revenue-Expenses

• Merchandising business

o (Sales revenue – COGS) = Gross Margin – Selling and Admin Expense = NET INCOME

• Shrinkage (expense) – loss of inventory from things like theft

Chapter 5

• Perpetual inventory system – tracks inventory coming in and out of the business continuously

(product cost, update while it happened)

• Period Inventory System – wait until the end of the period then find out how much inventory is

left ad assue hat is’t left as sold ad eod this (does’t ok eause it does’t

account for theft)

Chapter 10

• Product costs – happen in the factory and are treated as an asset

• Period costs – happen in the corporate office in this period

• If you are payig shippig to a seller it’s a period ost, if you are gettig it shipped to you it’s a

product cost

• Raw materials inventory – consists of money spent on raw materials

• Work in progress inventory (WIP) – consists of labor, and overhead

• Finished goods inventory – any costs added to WIP

• All of this stuff equals the product cost, everything else is a period cost and under retained

earnings as a selling and administration expense

Chapter 11

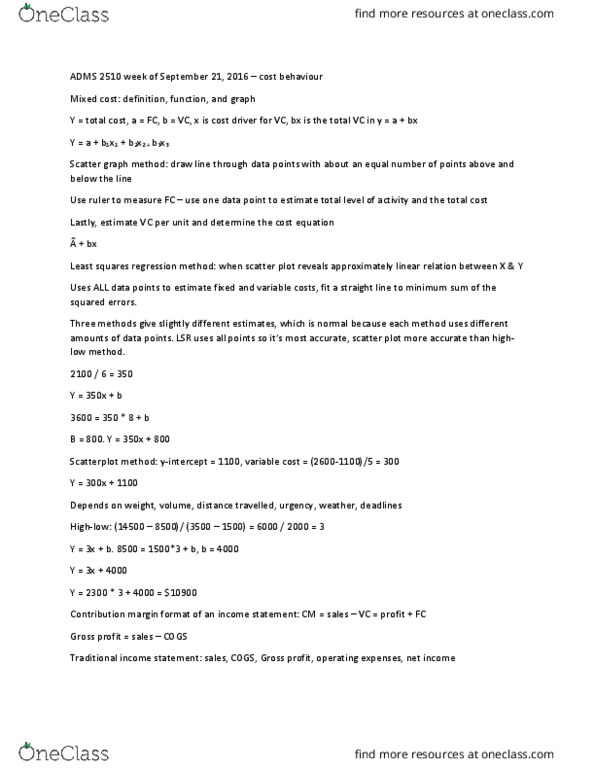

• Variable cost – a cost which changes in total as activity level changes (materials/ labor)

• Fixed cost – a cost which remains constant in total as activity changes (overhead)

• Contribution Margin – the income statement based on variable and fixed cost

• You can improve the CM by:

o Increase the sales price

o Decrease the variable cost

• TCM / # of units = CM/ unit

• Breakeven point – business sales turns out to be 0$ after expense

• When you increase volume average cost goes down because you are spreading out the fixed

cost over a larger amount of units

• Manufacturing process –

o Raw materials =>

o Work in Progress (WIP) =>

o Finished goods inventory =>

o COGS

find more resources at oneclass.com

find more resources at oneclass.com