AC 210 Study Guide - Final Guide: Stock Split, Corporate Finance, Under Armour

28 Apr 2017

School

Department

Course

Professor

Document Summary

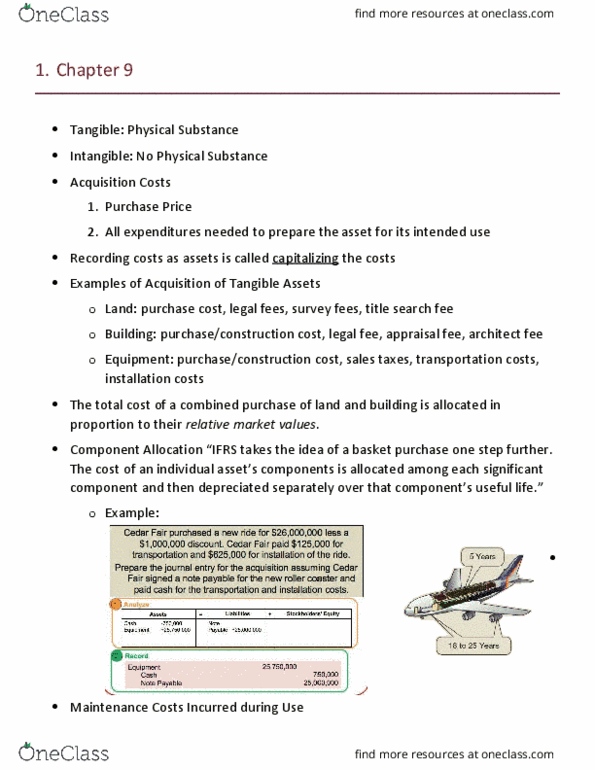

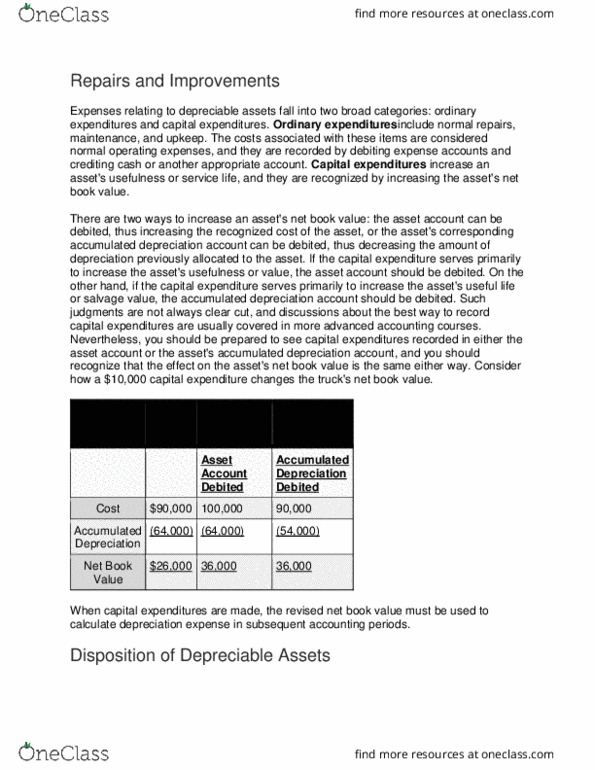

The cost of an i(cid:374)di(cid:448)idual asset"s (cid:272)o(cid:373)po(cid:374)e(cid:374)ts is allo(cid:272)ated among each significant component and then depreciated separately over that (cid:272)o(cid:373)po(cid:374)e(cid:374)t"s useful life. (cid:863: example: ceder fair purchase a new ride for ,000,000 less a ,000,000 discount. Ceder fair paid ,000 for transportation and ,000 for installation of the ride: analyze, assets: cash -,000 equipment +,000,000, liabilities: notes payable +25,000,000, record, credit, debit: ,000,000: maintenance costs incurred during use, ordinary repairs and maintenance (expense, relatively small, recurring expenditures that maintain normal operating condition, do not increase productivity, do not extend life beyond original estimate, extraordinary repairs. Replacements, and additions (capitalize: relatively large, infrequent expenditures such as major overhauls or replacements of major components, may extend useful life, may increase productivity or efficiency, cost allocation. Depreciation is a cost allocation process that matches costs of operational assets with periods benefited by their use: acquisition cost (cid:894)bala(cid:374)(cid:272)e heet(cid:895) (cid:894)cost allo(cid:272)atio(cid:374)(cid:895) expense (income. Statement: depreciation expense (cid:894)dep(cid:396)e(cid:272)iatio(cid:374) fo(cid:396) the (cid:272)u(cid:396)(cid:396)e(cid:374)t (cid:455)ea(cid:396)(cid:895) i(cid:374)(cid:272)o(cid:373)e.