AC 210- Midterm Exam Guide - Comprehensive Notes for the exam ( 119 pages long!)

12 Oct 2017

School

Department

Course

Professor

Document Summary

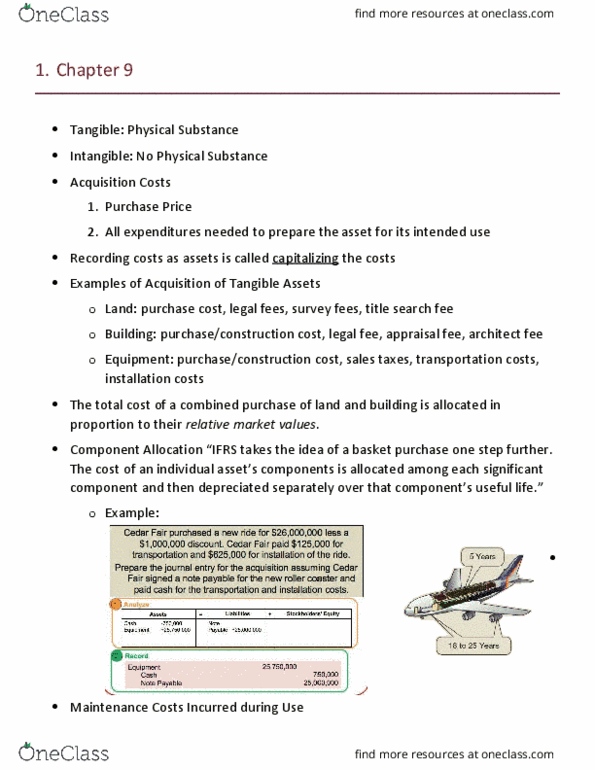

Acquisition costs: purchase price, all expenditures needed to prepare the asset for its intended use. Recording costs as assets is called capitalizing the costs. Examples of acquisition of tangible assets: land: purchase cost, legal fees, survey fees, title search fee, building: purchase/construction cost, legal fee, appraisal fee, architect fee, equipment: purchase/construction cost, sales taxes, transportation costs, installation costs. The total cost of a combined purchase of land and building is allocated in proportion to their relative market values. Component allocation ifrs takes the idea of a basket purchase one step further. The cost of an individual asset"s components is allocated among each significant component and then depreciated separately over that component"s useful life. : example: Depreciation is a cost allocation process that matches costs of operational assets with periods benefited by their use. Depreciation calculations require three amounts for each asset: acquisition cost, estimated useful life, estimated residual value. Depreciation methods: depreciable cost x depreciation rate = depreciation expense, straight-line.