ACC 925 Chapter Notes - Chapter 4: Canadian National Railway, Internal Control, Financial Statement

12 Oct 2016

School

Department

Course

Professor

Document Summary

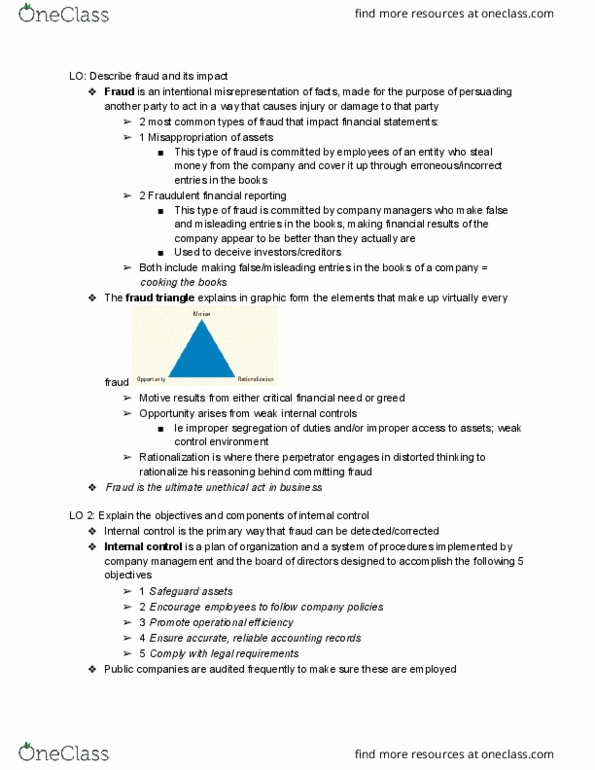

Fraud: is an intentional mispresenting of facts, made for persuading another party to act in a way that causes injury or damage to that party. The two types of fraud that impact financial statements: Misappropriation assets: the type of fraud is committed by employees of an entity who steal assets from their company and cover it up through false entries in the books. Examples: theft of inventory, falsifying invoices, forging or altering cheques. Fraudulent financial reporting: this type of fraud is committed by company managers who make false and misleading entries in the books, making financial results of the company appear to be better than they are. The purpose it to deceive investors and creditors to make decisions they otherwise would not have. Fraud triangle: made up of three components: motive. Results from either critical need or greed on the part of the person who commits the fraud (the perpetrator): opportunity.