COMMERCE 1AA3 Chapter Notes - Chapter 3: Debt Ratio, Current Liability, Financial Statement

7 Oct 2016

School

Department

Course

Professor

Document Summary

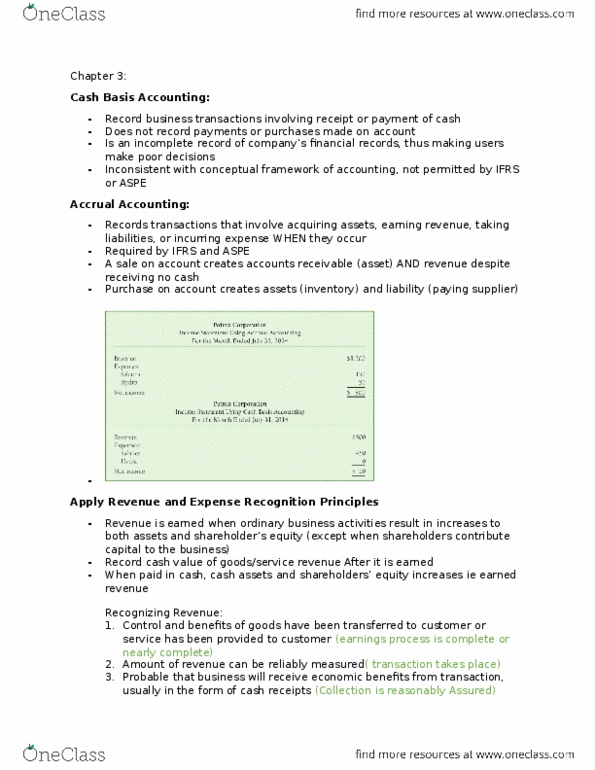

Record only business transactions involving receipt or payment of cash. If you make a ,000 sale on account, you don"t record the sale transaction until you receive the cash payment from the customer. The receipt or payment of cash is irrelevant; record business transactions when the business has acquired as asset, earned revenue, taken on a liability, or incurred an expense. If you make a ,000 sale on account, you record the account receivable (asset) and the revenue. Revenue recognition - conditions which must all be met before the revenue can be recognized. Revenue = increase to assets and shareholder"s equity (by increasing retained earnings: the control and benefits of the goods/service have been transferred/provided to the customer, the amount of the revenue can be reliably measured. It is probable that the economic benefits associated with the transaction will be received (usually in the form of cash)