COMMERCE 1AA3 Chapter Notes - Chapter 10: Canada Business Corporations Act, Chief Executive Officer, Bmo Nesbitt Burns

30 Nov 2016

School

Department

Course

Professor

Document Summary

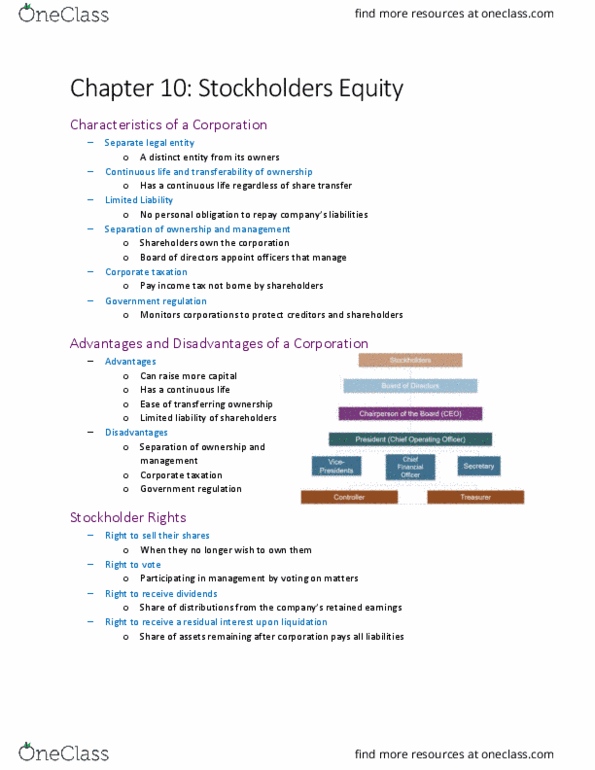

Learning objective one: explain the main features of a corporation. A corporation is a business entity formed under federal or provincial law. The federal or provincial government grants articles of incorporation, which consist of documents giving the governing body"s permission to form a corporation. A corporation is a distinct entity, an artificial person that exists apart from its owners, shareholders. Has many of the same rights as a person. Assets and liabilities in the business belong to the corporation, not the owners. Can enter into contracts, sue and be sued. Corporations have continuous lives regardless of changes in their ownership. Shareholders have limited liability for the corporation"s debts, so they have no personal obligation to repay the company"s liabilities. The most that a shareholder can lose on an investment in a corporation"s share is the cost of the investment. One of the most attractive features of the corporate form of organization.