COMMERCE 1AA3 Chapter Notes - Chapter 7: Book Value, Ddb Worldwide

7 Jan 2017

School

Department

Course

Professor

Document Summary

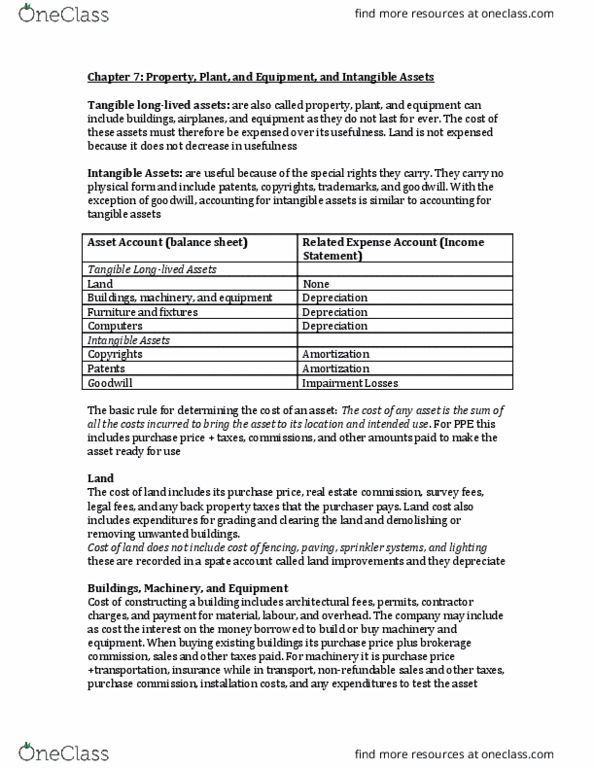

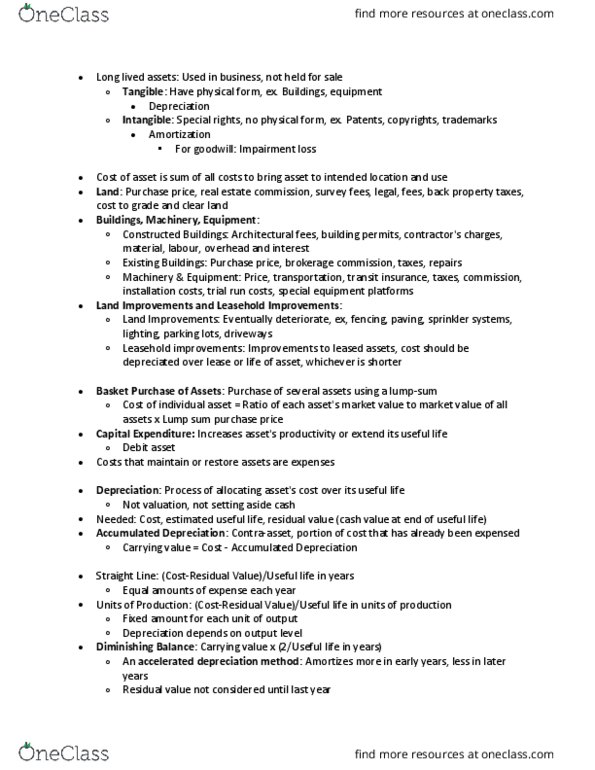

Physical substance property, plant & equipment, fixed assets. Rights, privileges, competitive advantages patents, copyrights, trademarks. Several assets purchased in a group at one price. Total cost allocated based on market value. Assets market value total market value = % of total market value x total cost. Two types of expenditures: capital expenditure increase productive life, operating efficiency, capacity of asset. Cost added to an asset account: revenue expenditure maintain productive capacity of the asset. Ddb and sym result in higher depreciation expense: lower earnings in early years and higher in later years. Remaining depreciable carrying amount (new) estimated remaining useful life. Carrying amount exceeds recoverable amount: caused by obsolescence, physical damage, and loss in market value. Asset recorded at cost when purchased but then measured at its fair value less any accumulated depreciation less any accumulated losses: fair value price at which the asset could be sold.