COMMERCE 1B03 Chapter Notes - Chapter 14: Financial Statement, Accounts Receivable, Debenture

11 Mar 2014

School

Department

Course

Professor

Document Summary

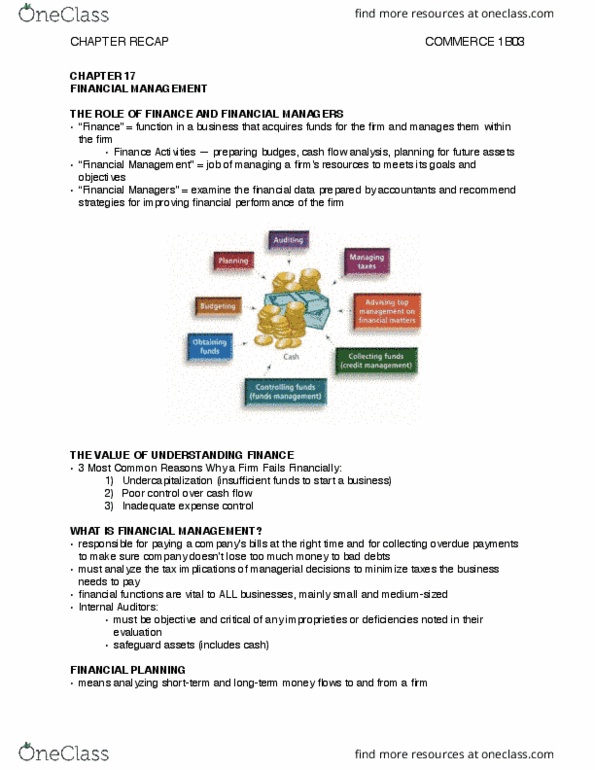

The function in a business that acquires funds for the firm and manages those funds within the firm. Activities include preparing budgets, doing cash flow analysis, and planning for the expenditure of funds on assets. The job of managing a firm"s resources so it can meet its goals and objectives. Managers who make recommendations to top executives regarding strategies for improving the financial strength of a firm. Common ways a firm fail financially: undercaptialization (lacking funds to start and run the business, poor control over cash flow. Financial planning is a key responsibility of the financial manager in a business. It involves three steps: forecasting both short-term and long-term financial needs, developing budgets to meet those needs, establishing financial control to see how well the company is doing what it set out to do. Forecast that predicts revenues, costs, and expenses for a period of one year or less.