COMMERCE 1B03 Chapter Notes - Chapter 6: Limited Liability Partnership, Sole Proprietorship, Limited Liability

18 Dec 2015

School

Department

Course

Professor

Document Summary

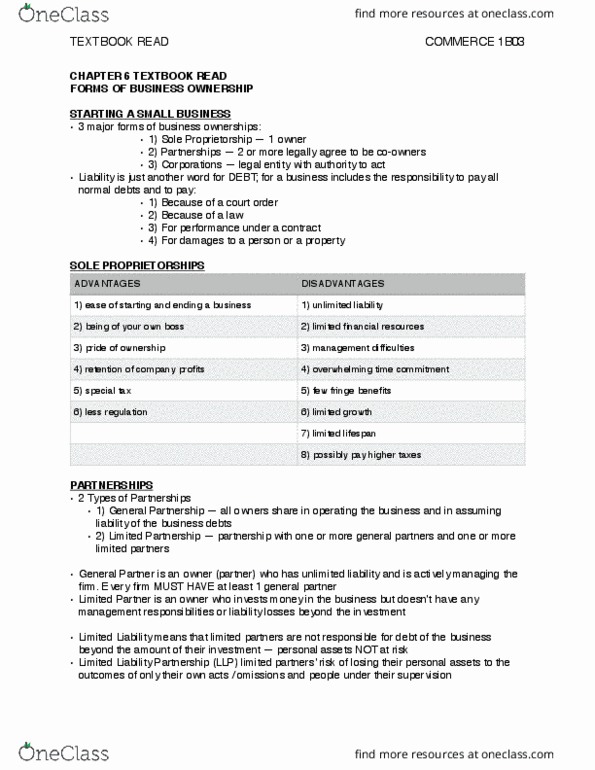

Ease of starting and ending the business. No special taxes all profits of a sold proprietorship are taxed at the personal. Pride of ownership. income of the owner, and the owner pays the normal personal income tax rate on that money. Unlimited liability the risk of potential losses: the responsibility of business owners for all of the debts of the business. Limited financial resources funds are limited to the funds that the sole owner can gather. Few fringe benefits no paid health insurance, no paid disability insurance, no sick leave, no vacation pay. Limited growth slow growth since it relies on its one owner for its creativity and funding. Limited lifespan the business dies when the sole proprietor dies. Possibly pay higher taxes if the business is profitable, it may be paying higher taxes than if it was incorporated as a canadian controlled private corporation (ccpc). A partnership is a legal form of business with two or more parties.