COMMERCE 2AB3 Chapter Notes - Chapter 6: Contribution Margin, Income Statement, European Cooperation In Science And Technology

12 Feb 2020

School

Department

Course

Professor

Document Summary

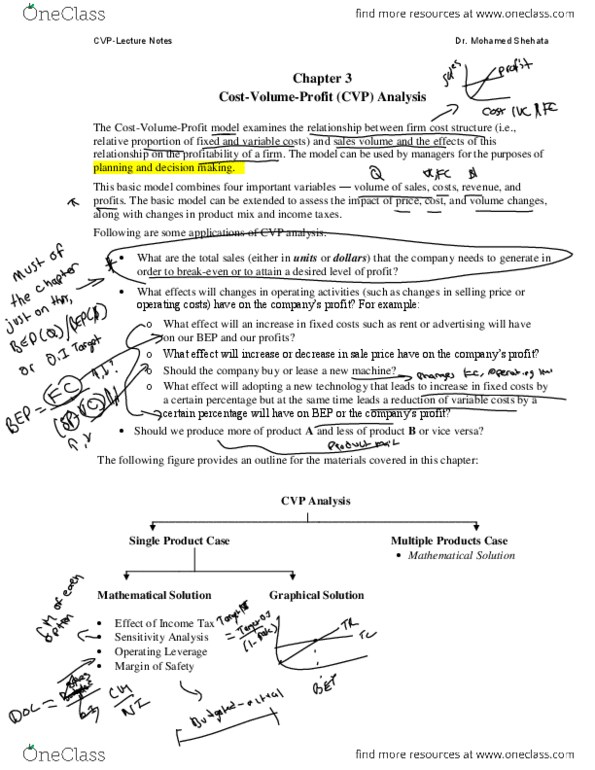

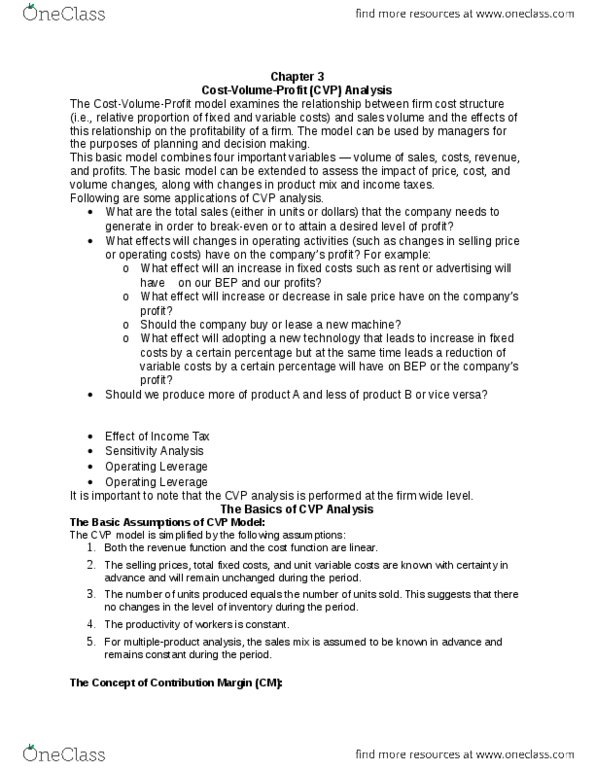

Cost-volume-profit (cvp) analysis is the study of the effects that changes in costs and volume have on a company"s profits. Classifies costs as variable or fixed and calculates a contribution margin. Contribution margin is the amount of revenue that remains after variable costs have been deducted. Traditional income statement does not classify costs as variable or fixed, and therefore would not report a contribution margin. Cvp income statement often shows both a total and a per-unit amount to help cvp analysis. The contribution margin per unit indicates that for every unit sold the firm will make the margin after variable costs have been deduced. Contribution margin ratio (contribution margin per unit divided by the unit selling price) of 40% means that sh. 40 of each sales dollar can be applied to fixed costs and contribute to operating income. Break-even point at this volume of sales, the company will realize no income and will suffer no loss.