ECON 1B03 Chapter Notes - Chapter 15: Deadweight Loss, Marginal Revenue, Imperfect Competition

29 Jul 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

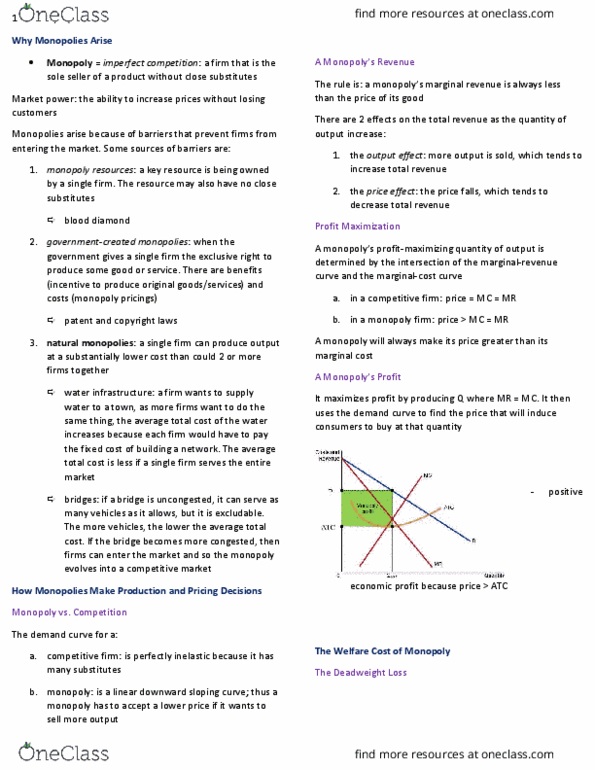

Monopoly = imperfect competition: a firm that is the. A monopoly"s revenue sole seller of a product without close substitutes. Market power: the ability to increase prices without losing customers. Monopolies arise because of barriers that prevent firms from entering the market. Some sources of barriers are: monopoly resources: a key resource is being owned by a single firm. The resource may also have no close substitutes. The rule is: a monopoly"s marginal revenue is always less than the price of its good. There are 2 effects on the total revenue as the quantity of output increase: 2. the output effect: more output is sold, which tends to increase total revenue the price effect: the price falls, which tends to decrease total revenue. Profit maximization: government-created monopolies: when the government gives a single firm the exclusive right to produce some good or service. There are benefits (incentive to produce original goods/services) and costs (monopoly pricings)