COMM 103 Chapter Notes - Chapter 13: Interest Expense, Angel Investor, Trade Credit

26 Jun 2018

School

Department

Course

Professor

PART THREE: MANAGING THE VALUE CHAIN

COMM 103

091317

(CHAPTER THIRTEEN) UNDERSTANDING BUSINESS FINANCES

TEXTBOOK SUMMATIVE

The chapter covers the following concepts:

●The Fundamentals of Financial Analysis

●The Revenue model

●Cost Structure and Cost Drivers

○Variable vs. Fixed Costs

○Breakeven Point Analysis

●Margin Requirements

●Cash Operating Cycle

●Capitalization requirements

○Sources of Funds

●Putting it All Together

●A Note Pertaining to NFPS

●Management Reflection - The Need for Capital

●Appendix - Advanced Topics Relation to BEP, Pricing, and The revenue Model Management

THE FUNDAMENTALS OF FINANCIAL ANALYSIS

The ability to analyze and draw conclusions regarding the financial integrity of an organization is

fundamental for a CFO to understand the organization’s current situation (revenue generation, sales

trends, etc) and the strategic and tactical planning decisions going forward. CFO’s draw conclusions

through FIVE KEY AREAS

1. Revenue Model

2. Cost Structure and Cost Drivers

3. Margin Requirements

4. Cash Operating Cycle (COC)

5. Capitalization Requirements (ROIC)

CFOS review these financial statements to determine how well the company is doing against its

objectives.

THE REVENUE MODEL

Dollars generated by the company can be calculated through the following formula:

Per Unit Selling Price x Quantity Sold = Sales Revenue

The revenue model analysis also allows us to ask questions, like:

●Which products within our portfolio are seeing increases in revenue? Likewise, which

products are seeing decreases?

PART THREE: MANAGING THE VALUE CHAIN

COMM 103

091317

●How much of our revenue is reliant on a single product?

○If there is only ONE product, than a company is 100% reliant on the success of that

product

○If there are MULTIPLE products, then work must be done to deduce the percentage

of revenue that arises from each product.

●Are sales predominantly driven as a result of selling to new customers, or existing

customers? What are the sales contribution of each?

●If we are relying on repeat sales for a product, what is the frequency of purchase for our

producer? Is it daily, weekly, annually, every three years, or so on?

●Are we dependant upon a small percentage of our customers for most of our sale? If so, who

are they and are sales from these customers increasing or decreasing?

●Is the selling price of our product being pushed down due to increasing competition? Are we

able to manage selling price reductions through contracts and/or other mechanisms;

thereby protecting further selling price declines?

●What about average revenue per customer transaction? Are we able to increase this by

bundling, packaging, or regrouping the way that we offer products and services?

Such questions can continue to grow depending on the nature of products one sells.

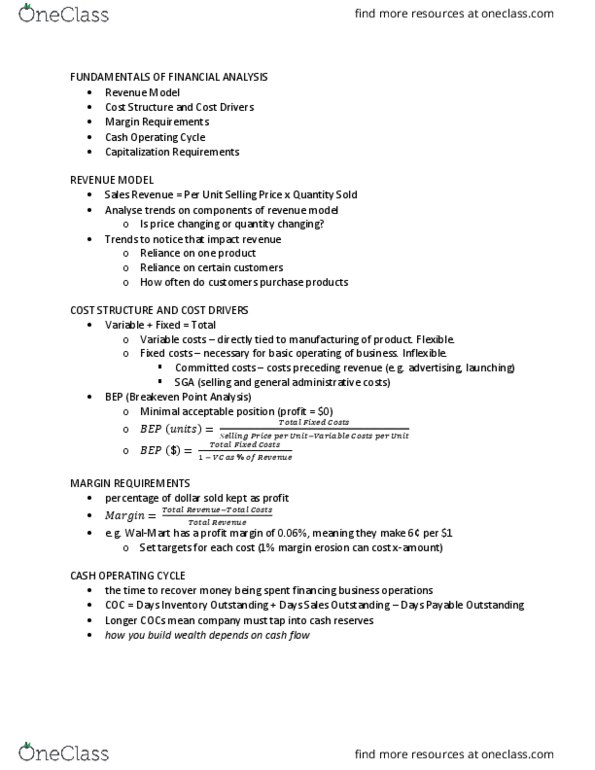

COST STRUCTURE AND COST DRIVERS

At its basic form an organization’s cost base is made up of total costs associated with delivering the

organization’s products or services to the market place.. These can include:

●The procurement of parts/resources

●Manufacturing costs

●Distribution costs

●Marketing and sales costs

●Administration costs

●Post-purchase service and support costs

TOTAL COST BASE FORMULA

Direct or Variable Costs + Indirect or Fixed Costs = Total Cost Base

In analysing the composition of an organization’s cost base, one can identify two fundamental

conclusions:

●The percentage of costs that are considered direct or variable costs vs those that are

considered indirect or fixed.

●The cost areas (if any) that make up a significant percentage of the overall cost base

VARIABLE COSTS (or “direct costs”) are costs that are directly tied to the manufacturing of a product

or the delivery of a service depending on the type of business being assessed. These will include:

●Cost of components or resources needed for product/service

●Cost of labour

●Cost of packaging and distribution

PART THREE: MANAGING THE VALUE CHAIN

COMM 103

091317

INDIRECT COSTS are those costs that, although not directly tied to the manufacturing or distribution

of a specific product, nonetheless exist as a result of conducting/operating one’s business. These

include:

●Insurance

●Utilities

●Interest expense on debt

●Administration costs

***It is important to note that fixed costs represent an expense that is uncontrollable in the near term;

meaning that managers have little ability to change its amount.

COMMITTED COSTS are another type of indirect cost that a company commits itself to within an

operating year, and are often spend in advance or at the front end of a manufacturing/sales cycle.

Examples of this would include:

●Marketing costs and advertising expenditures

●Software technology updates

●R&D costs

COST LADDER

TOTAL COST-BASE COMPOSITION

Document Summary

Management reflection - the need for capital. Appendix - advanced topics relation to bep, pricing, and the revenue model management. The ability to analyze and draw conclusions regarding the financial integrity of an organization is fundamental for a cfo to understand the organization"s current situation (revenue generation, sales trends, etc) and the strategic and tactical planning decisions going forward. Cfo"s draw conclusions through five key areas: revenue model, cost structure and cost drivers, margin requirements, cash operating cycle (coc, capitalization requirements (roic) Cfos review these financial statements to determine how well the company is doing against its objectives. Dollars generated by the company can be calculated through the following formula: Per unit selling price x quantity sold = sales revenue. The revenue model analysis also allows us to ask questions, like: If there is only one product, than a company is 100% reliant on the success of that product.