COMM 200 Chapter Notes - Chapter 13: Limited Liability Partnership, Sole Proprietorship, Corporate Tax

13 Mar 2014

School

Department

Course

Professor

Document Summary

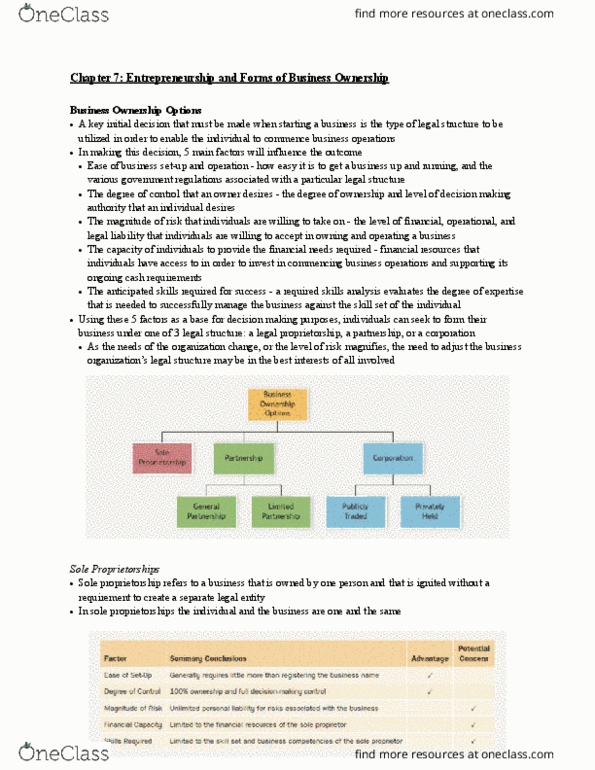

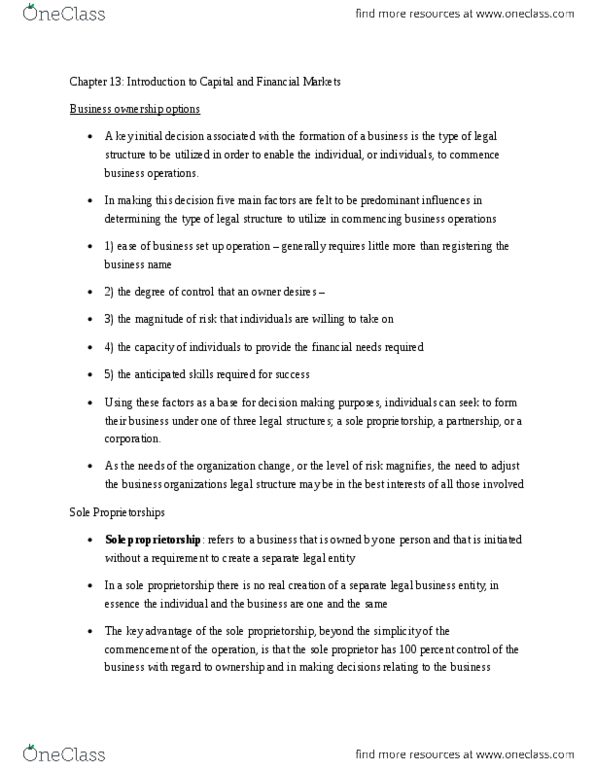

Using these factors as a base for decision-making, individuals can form their business under one of three legal structures: sole proprietorship, partnership, corporation business structure in the future. Sole proprietorship: the commencement of a business by a single individual: no real creation of a separate legal business entity; the individual and the business are the same. Partnership if other partners are unable to pay their portion of the partnership"s obligation. The general partner(s) assume full liability exposure on behalf of the partnership. Corporations: creates a distinct legal entity separate from its owners; established through. Corporations incorporation: incorporation can be done provincially or federally allowing the business to legally operate respectively in a province or throughout canada. Able to use the same business name in all provinces: however, it is also more expensive to set up, requires additional paper work and there are requirements associated with corporate governance.