COMM 200 Chapter Notes - Chapter 12: Profit Margin, Fixed Cost

18 Aug 2016

School

Department

Course

Professor

Document Summary

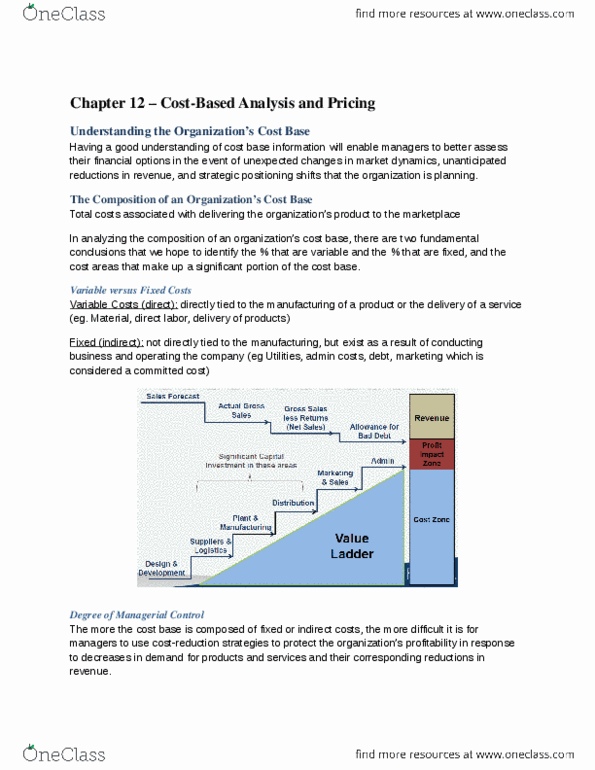

Costs that are directly tied to the manufacturing of a product or the delivery of a service depending on the type of business being assessed. Costs that are not directly tied to the manufacturing of a specific product or delivery of a specified service, nonetheless exist as a result of conducting our business and operating our company. Level of sales revenue or volume that is required for the organization to cover all of its cost. Addition to the manufacturers price that distributors add to the price of a product to ensure that their own direct and indirect costs are covered and that their profit margin is achieved. Reduction in the price of the product with the intent to stimulate the sale of the product over a defined period of time. Utilization of a premium price strategy in order to maximize the margin return on the sale of each individual unit of a particular product.