AFA 200 Chapter Notes - Chapter 4: Railways Act 1921

16 Jun 2017

School

Department

Course

Professor

Document Summary

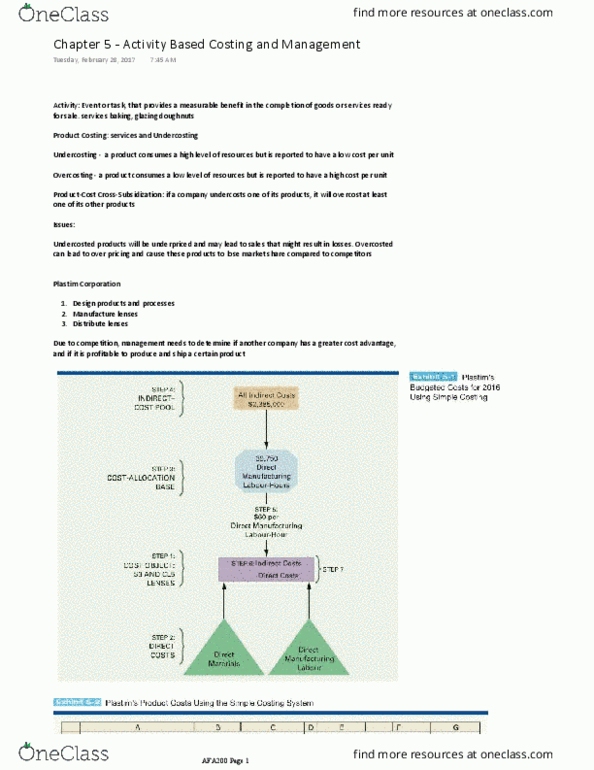

Cost object: an object that uses costs (like a product being made) Can be broad (all manufacturing plant costs) or narrow (costs of operating cutting machines. A way to group indirect cost/groups of indirect cost to cost object. I. e. it costs 500,000$ to run machines for 100,000 hours= per machine hour. Uses different amounts of resources vs other jobs. Cost object is masses of identical or similar units of a product/service. Total costs of producing an identical product/service / total number of units = per unit cost. Gives a close approximation of costs of various jobs throughout the year. Budgeted indirect cost rate= budgeted annual indirect costs/budgeted annual quantity of the cost allocation base. Traces direct costs to a cost object by using the actual direct cost rates x actual quantities of the direct cost inputs. Allocates indirect costs based on budgeted indirect cost rates x actual quantities of the cost allocation bases.