BUS 251 Chapter Notes - Chapter 4: Cash Flow, Net Income, Interest Rate

6 Apr 2018

School

Department

Course

Professor

Document Summary

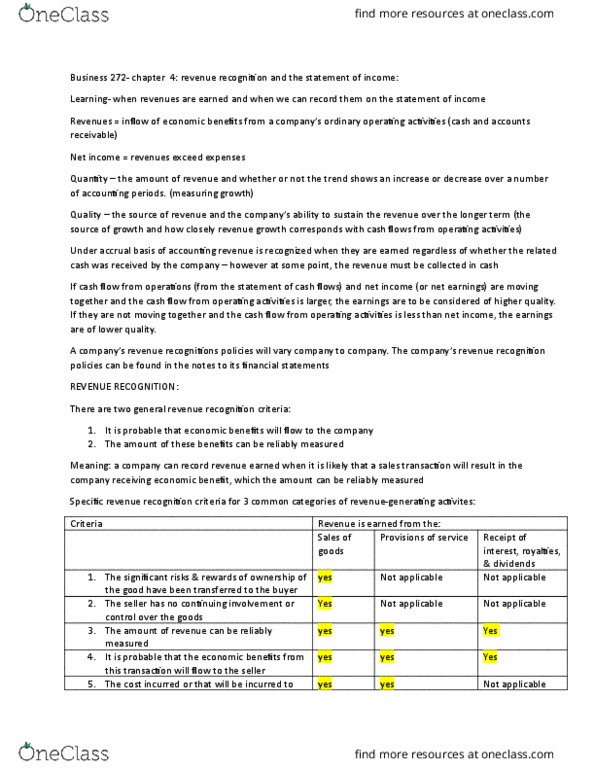

Chapter 4 revenue recognition and the statement of income. Why are a co(cid:373)pa(cid:374)y"s reve(cid:374)ue recog(cid:374)itio(cid:374) policies of sig(cid:374)ifica(cid:374)ce to users: use(cid:396)s (cid:374)eed to (cid:271)e a(cid:449)a(cid:396)e of the (cid:272)o(cid:373)pa(cid:374)(cid:455)"s (cid:396)e(cid:448)e(cid:374)ue (cid:396)e(cid:272)og(cid:374)itio(cid:374) poli(cid:272)ies so that the(cid:455) (cid:272)a(cid:374) (cid:373)ake informed judgements about reported revenues. When are revenues recognized: two general revenue recognition criteria. It is probable that economic benefits will flow to the company: the amount of these benefits can be reliably measured. Specific revenue recognition criteria by category of revenue-generating activity. When the title to the goods have been transferred to the customer, the risks and rewards of ownership of the goods has also been shifted. At the time of the sale, the selling price is agreed to by the seller and buyer, so the selling. The selling company usually has incurred all the costs by the time the goods are sold (transportation & selling costs). When selling on account, these costs can be estimated using historical data & industrial data.