BUS 251 Chapter Notes - Chapter 7: Consignor, Consignee, Vote Counting

15 Aug 2016

School

Department

Course

Professor

Document Summary

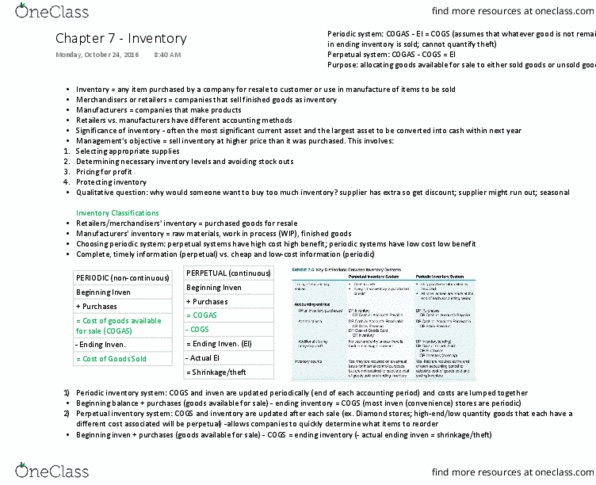

Inventory = any item purchased by company for resale to customers/used in manufacture of product that is then sold to customers. All companies (except service businesses) have inventory. Merchandiser/retailer = purchase inventory from others to sell at profit. Largest asset that will be converted to cash over next year. Management"s objective for inventory: sell it at higher price than company purchased it for: select suppliers. Consider location, time, delivery: decide how much inventory to purchase from supplier. Do not want too much (will become obsolete), but also want to meet customer demand. Raw materials = all items required to make product. Work-in-process = used to record costs of products that have been stared but not completed at end of accounting period. Incl. cost of raw materials, labour costs, overhead costs (other manufacturing costs) incurred as product is being made. Once manufacturing process complete, full cost of making product transferred from work-in-