BUS 251 Chapter Notes - Chapter 2: International Accounting Standards Board, International Financial Reporting Standards, Financial Statement

6 Apr 2018

School

Department

Course

Professor

Document Summary

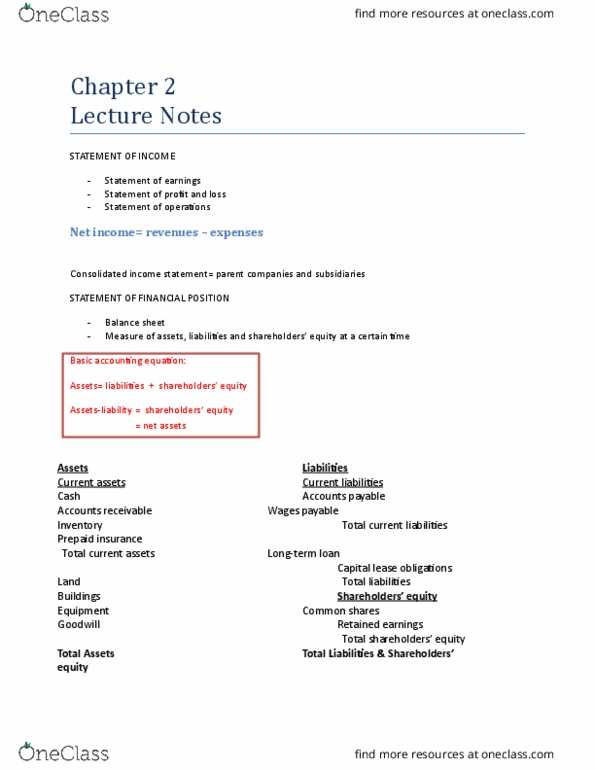

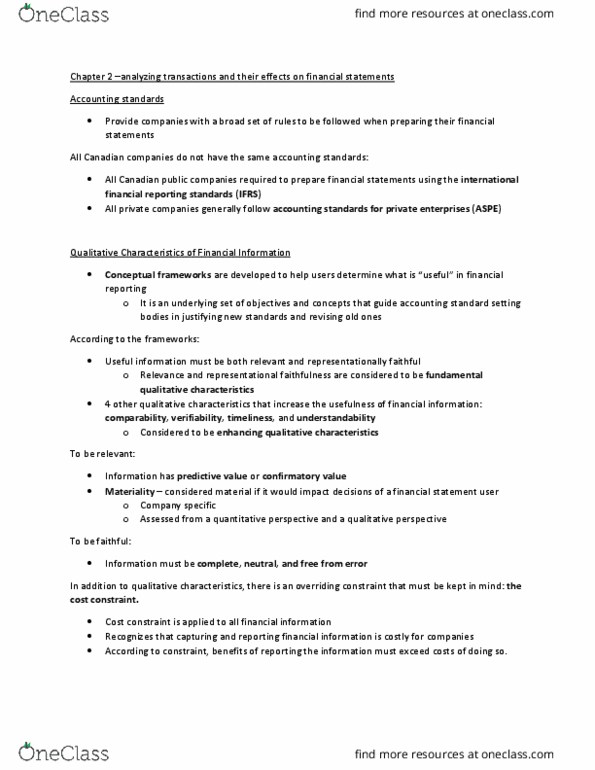

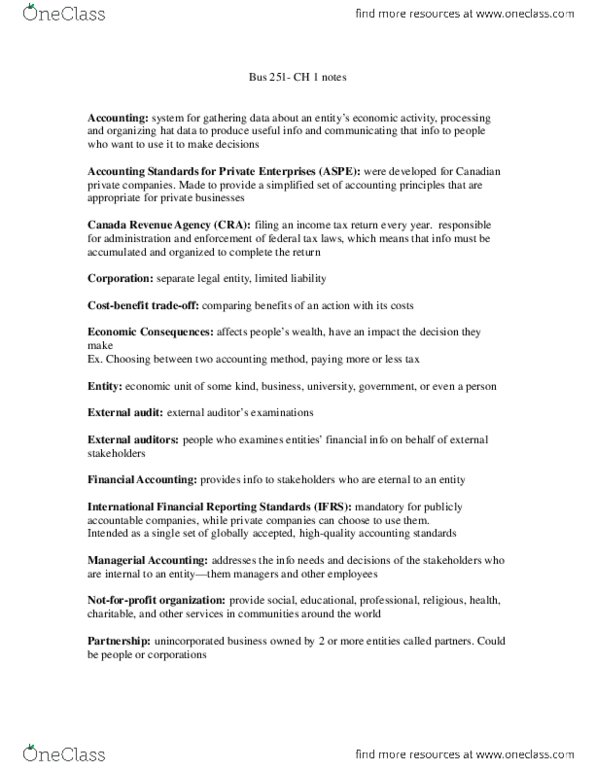

Chapter 2 analyzing transactions and their effects on financial statements. International financial reporting standards (ifrs: private companies follow accounting standards for private enterprises (aspe, the canadian accounting standards board (acsb) is responsible for developing and establishing the accounting standards for canadian companies. International accounting standards board (iasb) is responsible for the ongoing development of. How do the standard setters determine what constitutes useful financial info: conceptual frameworks: an underlying set of objectives and concepts that guide accounting standard-setting bodies in justifying new standards and revising old ones. Straight-line depreciation expense = (cid:2899)(cid:2928)(cid:2919)(cid:2917)(cid:2919)(cid:2924)a(cid:2922) c(cid:2925)(cid:2929)(cid:2930) e(cid:2929)(cid:2930)(cid:2919)(cid:2923)a(cid:2930)(cid:2915)(cid:2914) (cid:2902)(cid:2915)(cid:2929)(cid:2919)(cid:2914)(cid:2931)a(cid:2922) (cid:2906)a(cid:2922)(cid:2931)(cid:2915) E(cid:2929)(cid:2930)(cid:2919)(cid:2923)a(cid:2930)(cid:2915)(cid:2914) (cid:2905)(cid:2929)(cid:2915)(cid:2916)(cid:2931)(cid:2922) l(cid:2919)(cid:2916)(cid:2915: the number of columns that can be included within the template is limited when printing it out, e. g. many different types of inventory but unable to do account for separately with this template. Lack of specific revenue, expense, and dividends declared accounts they are recorded directly to retained earnings.