BUS 254 Chapter Notes - Chapter 2: Quality Control, Iso 9000, Statistical Process Control

26 Sep 2013

School

Department

Course

Professor

3

BUS 254 Full Course Notes

Verified Note

3 documents

Document Summary

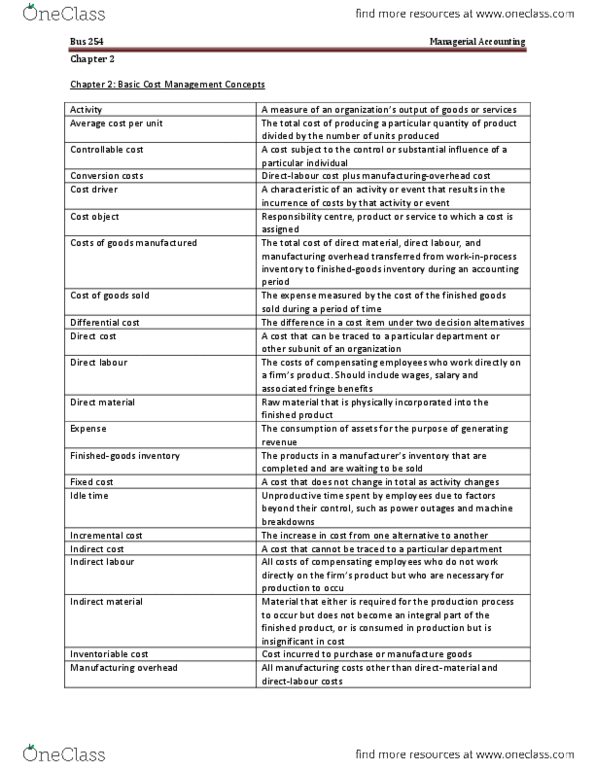

Factory labour costs that can be traced easily to individual units of product: indirect labour = cannot be traced easily to individuals. Include cost of janitors, supervisors, security guards, etc. Essential for production but not part of it: benefits (pensions) for direct labour are added in the direct labour costs. ** idle time could be part of direct labour or manufacturing overhead depending on how manager allocates it ** ** same with overtime premiums (usually half of pay x time) ** Matching principle = cost incurred to generate revenue should be expensed in same period as revenue generated. On the balance sheet: manufacturing companies have 3 categories of inventory: raw material, work in process, and finished goods; while merchandising companies only have 1. For manufacturing companies: cost of goods sold = beginning inventory + purchases ending inventory, cost of goods sold = beginning finished goods inventory + cost of goods manufactured ending finished goods inventory.