ACCTG322 Chapter Notes - Chapter 8: Total Absorption Costing, Earnings Before Interest And Taxes, Sorption

8 Apr 2014

School

Department

Course

Professor

Document Summary

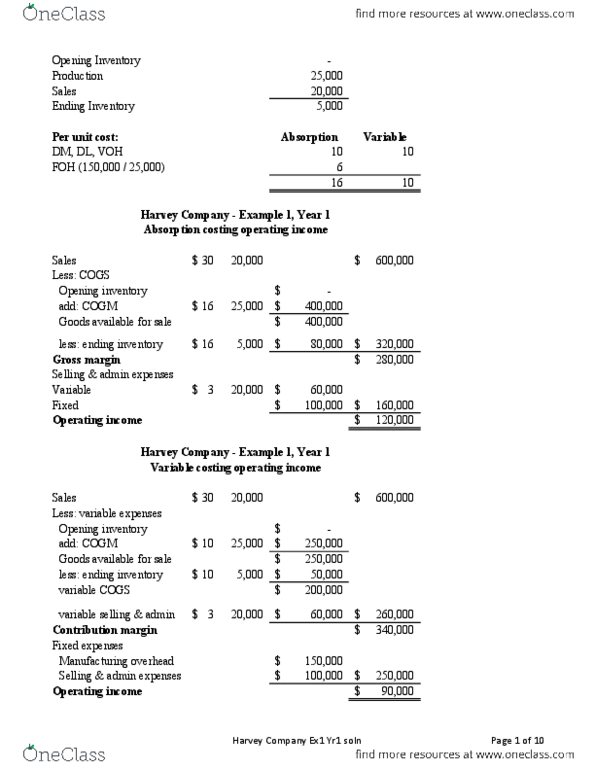

Exercise 8-9: sales (40,000 units . 75 per unit) . Variable cost of goods sold (40,000 units per unit*) Variable selling and administrative expenses (40,000 units per unit) . : the difference in operating income can be explained by the ,000 in fixed manufacturing overhead deferred in inventory under the absorption costing method: Add: fixed manufacturing overhead cost deferred in inventory under ab- sorption costing: 10,000 units per unit in fixed manufacturing over- head cost . Problem 8-10: the unit product cost under the variable costing approach would be computed as follows: With this figure, the variable costing income statements can be prepared: Variable cost of goods sold @ per unit Operating income (loss) : variable costing operating income (loss) Add: fixed manufacturing overhead cost deferred in in- ventory under absorption costing (5,000 units per unit) Deduct: fixed manufacturing overhead cost released from inventory under absorption costing (5,000 units. Fixed manufacturing overhead (640,000 40,000 units)