ACCT 2230 Chapter Notes - Chapter 5: Activity-Based Costing, Historical Cost, Cost Driver

20 Oct 2014

School

Department

Course

Professor

Document Summary

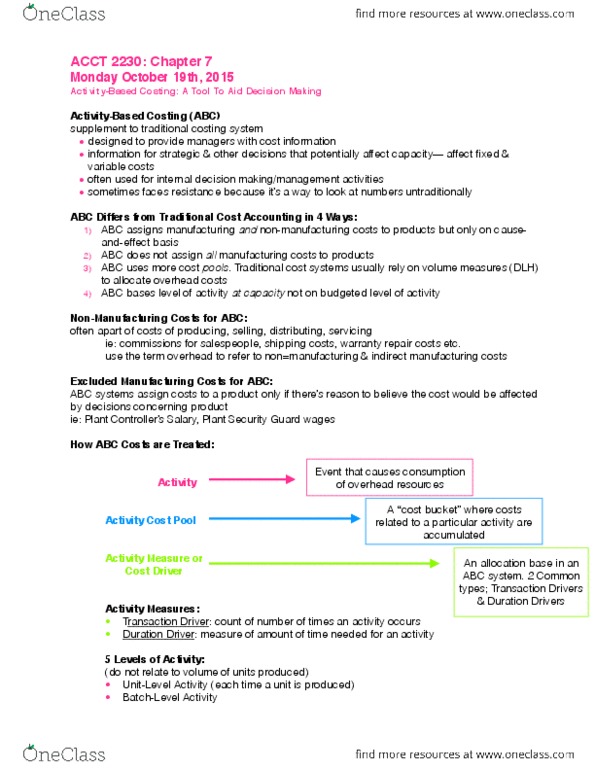

Activity-based costing (abc costing): a costing method based on activities that is designed to provide managers with cost information for strategic & other decisions that potentially affect capacity & fixed costs as well as variable costs. Usually used as supplement to other accounting cost system (this would just be for internal decision making) Abc accounting is designed for use in internal decision making. In abc costing, products are assigned all of the overhead costs (non-manufacturing & manufacturing) that they can reasonably be supposed to have caused we will be determining entire cost of product not just its manufacturing cost. In abc costing a cost is assigned to a product only if there is a good reason to believe that the cost would be affected by decisions concerning the product. Costs that are unaffected byproduct-related decisions are period costs in abc costing. Cost pools, allocation bases, & activity based costing: Activity: an event that causes the consumption of overhead resources.