ECON 2560 Chapter Notes - Chapter 16: Tax Shield, Financial Distress, Capital Structure

30 Jul 2013

School

Department

Course

Professor

Document Summary

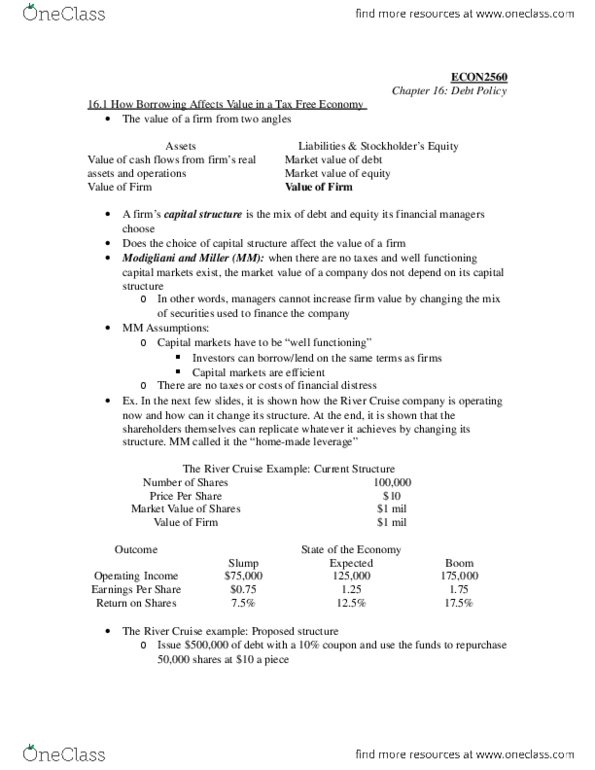

How borrowing affects value in a tax-free econmomy. Capital structure: a firm"s mix of long-term financing. If the fir changes the capital structure, overall value shouldn"t change. Financial managers cant increase value by changing the mix of securities used to finance the company. This has some assumptions such as capital markets are well-functioning (investors can trade securities without restrictions & can borrow and lend on same terms as firm) and that capital markets are efficient. Also assumes there aren"t any distorting taxes and ignores costs encountered if a firm borrows too much an lands in financial distress. The firm"s capital structure decision can matter if these assumptions are not true. As long as investors can borrow or lend on their own account on the same terms as the firm, they aren"t going to pay more for a firm that has borrowed on their behalf. The value of the firm after restructuring must be the same as before.