AFM102 Chapter Notes - Chapter 5: Contribution Margin, Fixed Cost, Variable Cost

13 Nov 2013

School

Department

Course

Professor

Document Summary

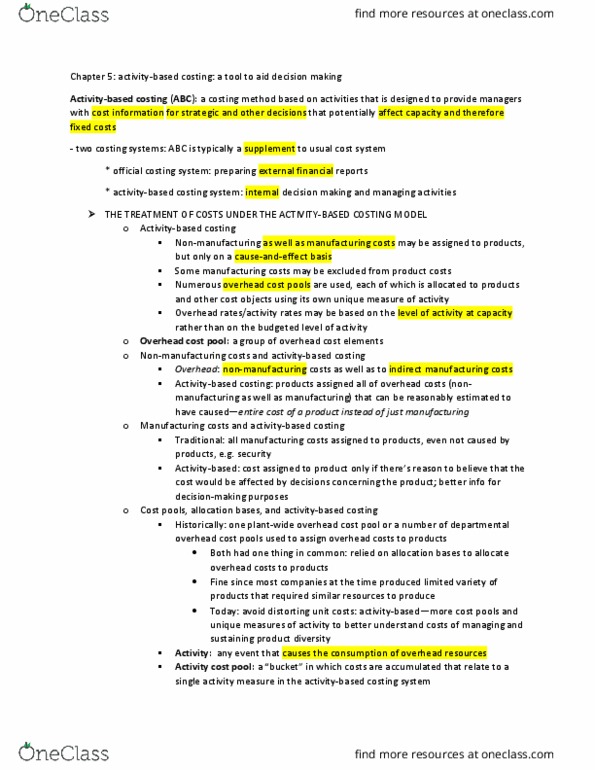

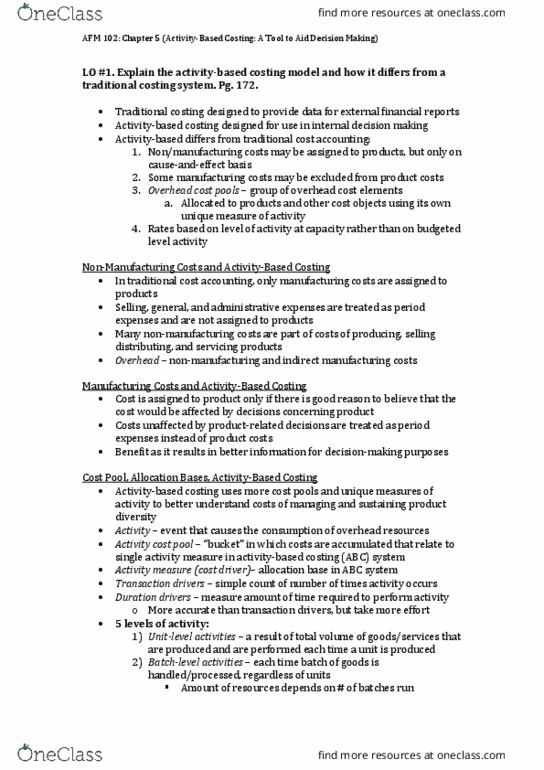

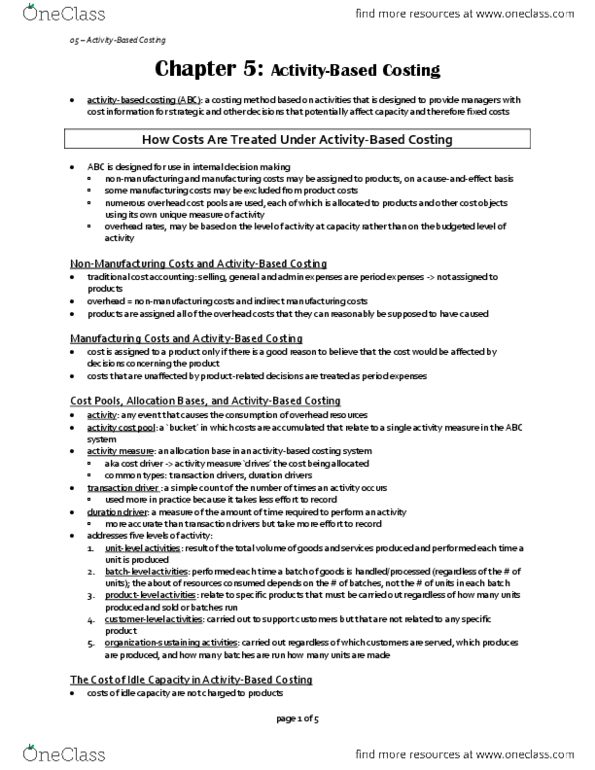

A costing method based on activities that is designed to provide managers with cost information for strategic and other decisions that potentially affect capacity and therefore fixed costs. Overhead refers to all costs including non-manufacturing costs. In activity-based costing, a cost is assigned to a product only if there is good reason to believe that the cost would be affected by decisions concerning the product. Costs that are unaffected by product-related decisions are treated as period expenses instead of product costs. Activity: any event that causes the consumption of overhead resources. Activity cost pool: a bucket in which costs are accumulated that relate to. Activity measure: an allocation base in an activity-based costing system; a single activity measure in the activity-based costing system ideally a measure of the amount of activity that drives the costs in an activity cost occurs activity. Transaction driver: a simple count of the number of times an activity.