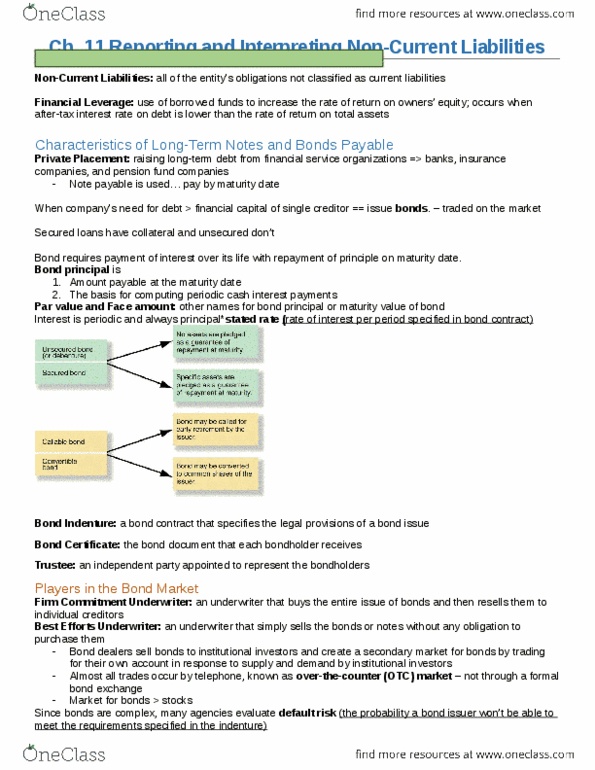

AFM101 Chapter Notes - Chapter 11: Market Rate

26 Jun 2018

School

Department

Course

Professor

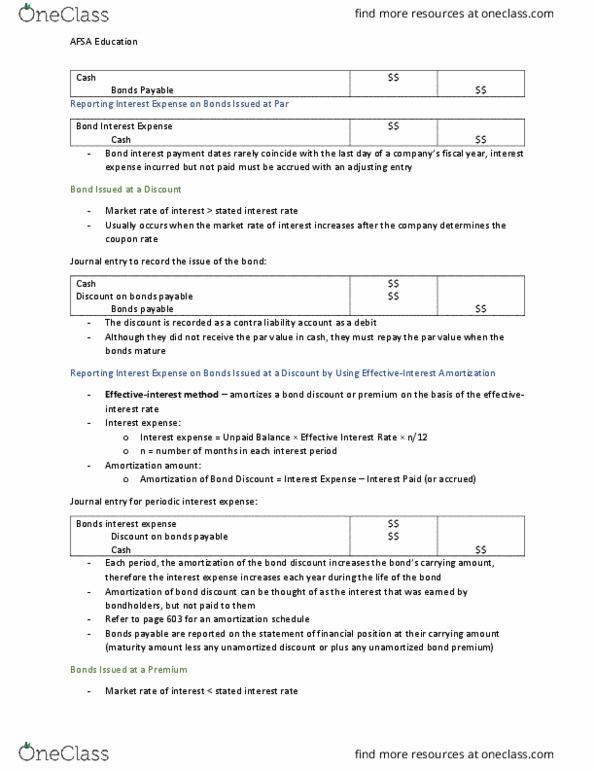

AFSA Education

o Cash interest payments – payments are computed by multiplying the principal amount

times the coupon rate. The bond contract specifies if the payments are made quarterly,

semi-annually or annually

Coupon rate – stated rate of interest on bonds

- The market determines the current cash equivalent of future interest and principal payments by

using present value concepts (from chapter 10)

- Present value of the bond = present value of the principal + present value of the interest

payments

- Market interest rate aka yield or effective-interest rate – the current rate of interest on a debt

when incurred, it should be used in computing the present value

- Present value can be the same as par, above par (premium) or below par (discount)

- Bond premium – the difference between the selling price and par when the bond is sold for

more than par

- Bond discount – the difference between the selling price and par when the bond is sold for less

than par

How to Calculate Present Value of Principal

𝑃𝑟𝑒𝑠𝑒𝑛𝑡 𝑉𝑎𝑙𝑢𝑒 = 𝑃

(1 + 𝑖)

- P = Principal

- i = the market interest rate per period (may not be the annual rate)

- n = number of compounding periods

Or, if you have the table of values:

𝑃𝑟𝑒𝑠𝑒𝑛𝑡 𝑉𝑎𝑙𝑢𝑒 = 𝑃 × 𝑣𝑎𝑙𝑢𝑒 𝑓𝑟𝑜𝑚 𝐴𝑝𝑝𝑒𝑛𝑑𝑖𝑥 10𝐶. 1 𝑢𝑠𝑖𝑛𝑔 𝑖 𝑎𝑛𝑑 𝑛

How to Calculate Present Value of an Ordinary Annuity

𝑃𝑟𝑒𝑠𝑒𝑛𝑡 𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝐴𝑛𝑛𝑢𝑖𝑡𝑦 = 𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑝𝑎𝑖𝑑 ×

1 − 1

(1 + 𝑖)

𝑖

- Interest paid = interest paid each period (cash paid) *this uses stated interest rate

- i = the market interest rate per period

- n = number of compounding periods

Or, if you have the table of values:

𝑃𝑟𝑒𝑠𝑒𝑛𝑡 𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝐴𝑛𝑛𝑢𝑖𝑡𝑦 = 𝑖𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑝𝑎𝑖𝑑 × 𝑣𝑎𝑙𝑢𝑒 𝑓𝑟𝑜𝑚 𝐴𝑝𝑝𝑒𝑛𝑑𝑖𝑥 10𝐶. 2 𝑢𝑠𝑖𝑛𝑔 𝑖 𝑎𝑛𝑑 𝑛

Bonds Issued at Par

- Market rate of interest = stated interest rate

- When effective rate of interest = stated rate of interest, present value of the future cash =

bond’s par value

- On the date of issue, bond liabilities are recorded at the present value of future cash flows

Journal entry to record the issue of the bond:

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Afsa education: cash interest payments payments are computed by multiplying the principal amount times the coupon rate. The bond contract specifies if the payments are made quarterly, semi-annually or annually. Coupon rate stated rate of interest on bonds. The market determines the current cash equivalent of future interest and principal payments by using present value concepts (from chapter 10) Present value of the bond = present value of the principal + present value of the interest payments. Market interest rate aka yield or effective-interest rate the current rate of interest on a debt when incurred, it should be used in computing the present value. Present value can be the same as par, above par (premium) or below par (discount) Bond premium the difference between the selling price and par when the bond is sold for. Bond discount the difference between the selling price and par when the bond is sold for less more than par than par.