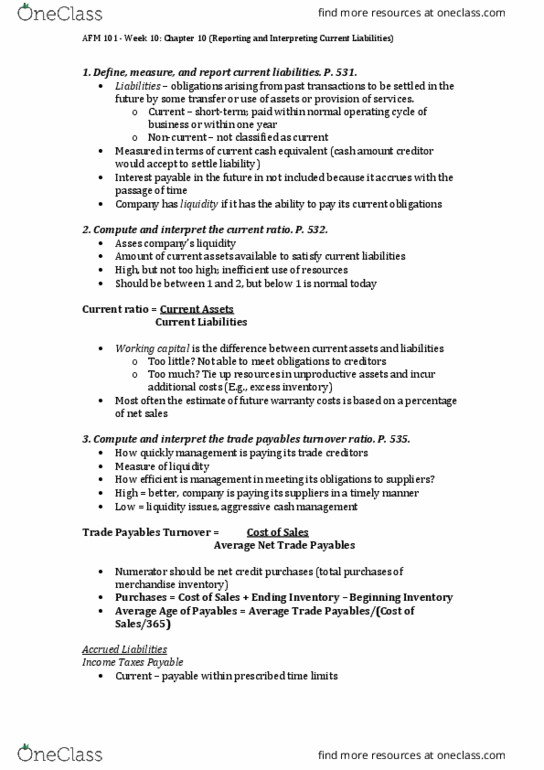

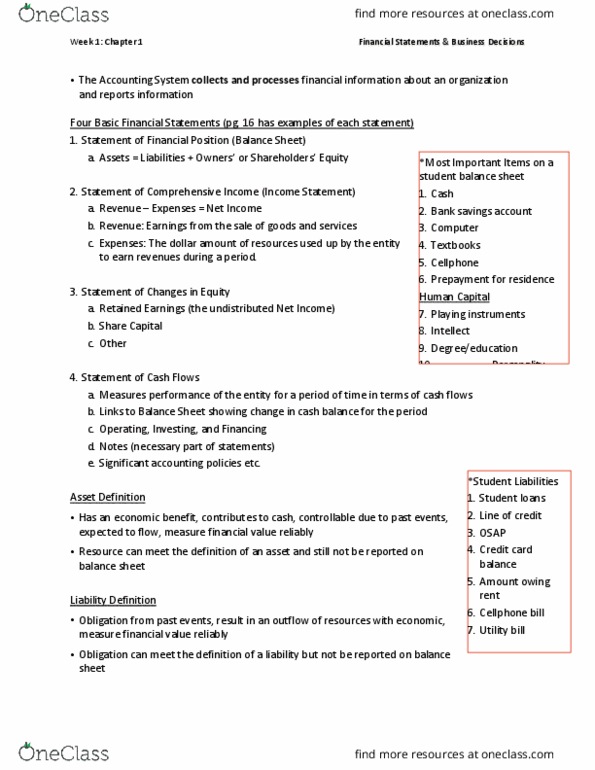

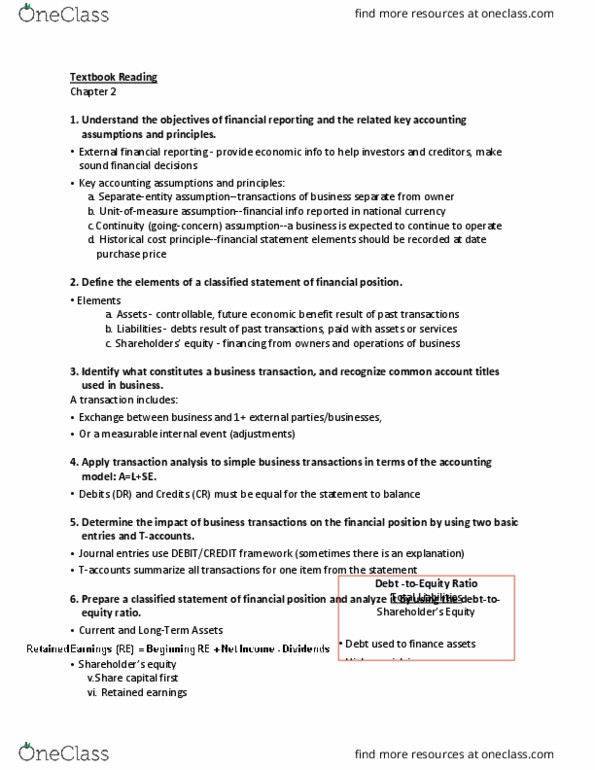

AFM121 Chapter Notes - Chapter 3: Accrual, Financial Statement, Income Statement

Document Summary

Get access

Related Documents

Related Questions

Ravenna Company is a merchandiser that uses the indirect methodto prepare the operating activities section of its statement ofcash flows. Its balance sheet for this year is as follows: |

| Ending Balance | Beginning Balance | ||

Cash | $ | 52,800 | $ | 62,700 |

Accounts receivable | 45,100 | 48,400 | ||

Inventory | 60,500 | 55,000 | ||

Total current assets | 158,400 | 166,100 | ||

Property, plant, and equipment | 165,000 | 154,000 | ||

Less accumulated depreciation | 55,000 | 38,500 | ||

| ||||

Net property, plant, and equipment | 110,000 | 115,500 | ||

Total assets | $ | 268,400 | $ | 281,600 |

| ||||

Accounts payable | $ | 35,200 | $ | 62,700 |

Income taxes payable | 27,500 | 30,900 | ||

Bonds payable | 66,000 | 55,000 | ||

Common stock | 77,000 | 66,000 | ||

Retained earnings | 62,700 | 67,000 | ||

| ||||

Total liabilities and stockholdersâ equity | $ | 268,400 | $ | 281,600 |

During the year, Ravenna paid a $6,600 cash dividend and it solda piece of equipment for $3,300 that had originally cost $6,600 andhad accumulated depreciation of $4,400. The company did not retireany bonds or repurchase any of its own common stock during theyear. |

1. | What is the amount of the net increase or decrease in cash andcash equivalents that would be shown on the companyâs statement ofcash flows? |

3. | How much depreciation would the company add to net income on itsstatement of cash flows? |

5-a. | What is the amount and direction (+ or â) of the accountsreceivable adjustment to net income in the operating activitiessection of the statement of cash flows? |

5-b. | What does this adjustment represent? | ||||||

|

7-a. | What is the combined amount and direction (+ or â) of theinventory and accounts payable adjustments to net income in theoperating activities section of the statement of cash flows? | ||||||

7-b. | What does this amount represent? | ||||||

|

| Anderson Accounting Services LLC provides accounting and tax preparation and consulting services. Sometimes customers only wish to have financial statements and/or tax returns prepared. Sometimes customers bundle accounting and tax preparation with consulting services (to be provided over a period of time). Sometimes customers only wish to have consulting services provided over a period of time. Because Anderson is a service firm there is no cost of goods sold associated with their services. | ||||||||

| Customer is Civic Corporation | 1 | |||||

| Tax consulting begins on November 1st and runs through the next April | 11/1/X7 | |||||

| Date of contract | 11/1/X7 | |||||

| Length of consulting services | 6 months | months | ||||

| Tax return preparation occurs over the period February through April of | 20X8 | |||||

| Length of tax prepartion | 3 months | |||||

| Price of tax preparation to be allocated over the return preparation period | $ 2,000 | stand alone price | ||||

| Price of consulting services to be allocated over consulting period | $ 5,000 | stand alone price | ||||

| Customers are charged a lesser amount as follows for both tax and consulting | $ 6,000 | |||||

| Anderson Accounting Services LLC's current year end | 12/31/X7 | |||||

| Customers pay at the contract date for BOTH the consulting and tax preparation services. | ||||||

What are the performance obligations in the contract?

| A. | Tax preparation services | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| B. | Tax preparation services and tax consulting services | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| C. | Unable to determine | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| D.Tax consulting services QUESTION 3 Determine the transaction price that should be allocated to the consulting services.

QUESTION 4 Calculate the total revenue that should be recognized in the current accounting period.

QUESTION 5 What is the total amount in the deferred revenue account(s) at the end of the current accounting period?

QUESTION 6 What is the total amount of revenue that should be recognized in the NEXT accounting period period?

QUESTION 7 The following journal entry has what impact on the income statement? Debit Cash XXX Credit Deferred Revenue XXX

QUESTION 8 The following journal entry has what impact on the income statement? Debit Cash XXX Credit Accounts Receivable XXX

QUESTION 9

QUESTION 10

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||