AFM291 Chapter Notes - Chapter 4: Revenue Recognition, Financial Statement, Disclose

18 May 2018

School

Department

Course

Professor

AFM291- Chapter 4: Revenue Recognition

• Recognition: presenting an item in the financial statements rather than just disclosing in notes

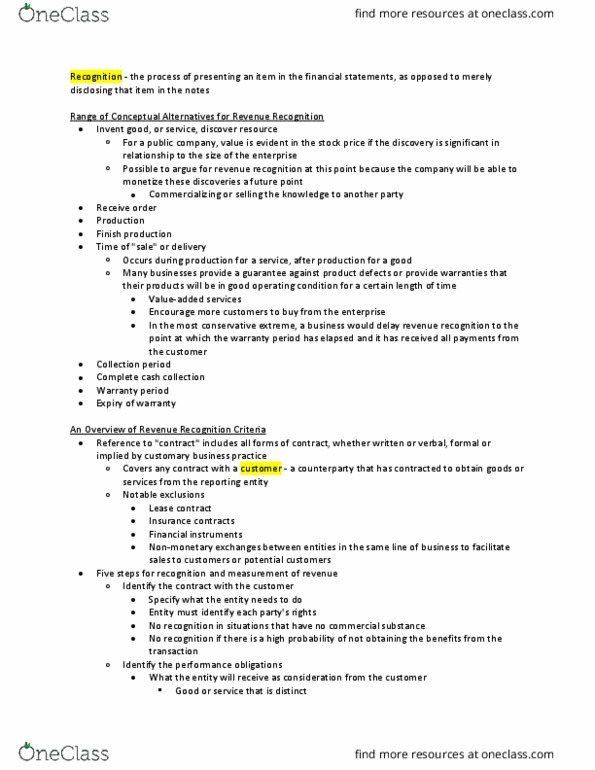

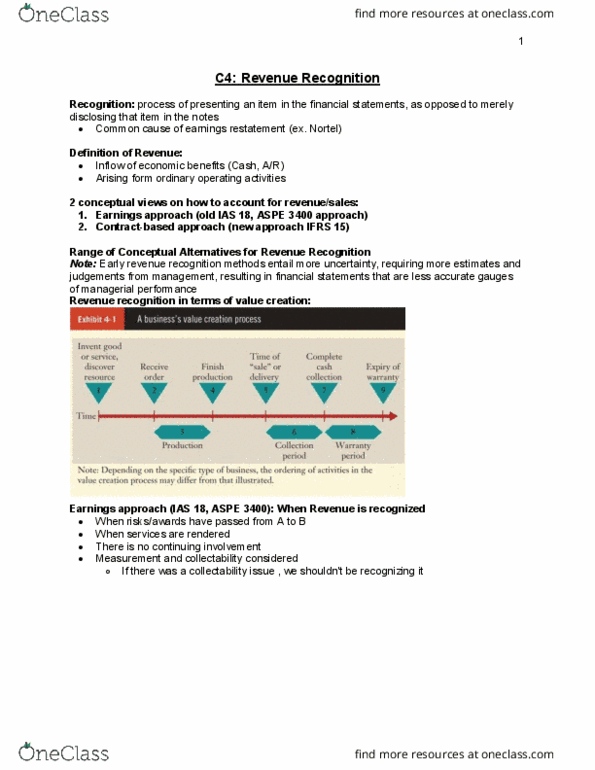

• Many businesses create warranty for their products and at the most conservative extreme, a

business would delay revenue recognition to the point at which the warranty period has elapsed

and it ahs received all payments from the customer.

• Early revenue recognition methods entail more uncertainty which is less reliable and less useful.

An Overview of revenue Recognition

• Criteria for revenue recognition is revenue from contracts with customers (written, verbal,

formal). The standard covers any contract with a customer- a counterparty that has contracted

to obtain goods or service from the reporting entity.

o Exclusions:

▪ Lease contracts, insurance contracts, financial instruments, non-monetary

exchanges between entities in the same line of business to facilitate sales

customers

• Five steps for revenue recognition:

1) Identify the contract with the customer

2) Identify the performance obligations

3) Determine the transaction price

4) Allocate the transaction price to performance obligations

5) Recognize revenue in accordance with performance

Revenue Recognition Criteria: A More Detailed Look

1. Identify the contract

• A) the parties to the contract have approved the contract and are committed to perform

• B) a Idetif eah part’s rights regardig the goods or services to be transferred

• C) can identify the payment terms

• D) the contract has commercial substance

• E) it is probable the entity will collect the consideration to which it will be entitled for the service

provided.

2. Identify the Performance Obligation

• Separating performance obligations if goods are distinct from one another.

a) Distinct if:

o Customer can benefit from goods on its own or together with other available resources

(checking to see if it is inherently capable of being distinct)

o Good/service is separately identifiable from other promises in the contract (considers

distinctiveness in the context of the contract)

find more resources at oneclass.com

find more resources at oneclass.com

E.g. bricks or piping for building can provide benefit on its own or together, however, it does’t ) as the

individual components have the purpose of delivering a completed building

b) A series of distinct goods or services that are substantially the same and that have the same

pattern of transfer to the customer e.g. deliver 5000 tones of aluminum to a customer each

month over a 24-month period.

3. Determine the transaction price

A. Non- cash consideration

• Seller needs to estimate the fair value of the non-cash consideration

o E.g. Buy a new car. Trade- in old car estimated to be $7,500 and pay another

$20,000. Transaction price is $27,500

• Sometimes non-ash osideratio/estiate is’t reliale, so e use the stad-alone selling

price

o E.g. new car is $28,000 and you pay $20,000 in cash, that would mean that the fair value

of the old car is $8000

• Non-oetar trasatios of assets that are’t a ai reeue geeratig atiit are ot

contracts with customers and fall outside scope of IFRS15

B. Significant financing component

• If the payment for a good you provided will not be collected until two years ($121,000), you

would have to record the PV of this value (say 10% interest) $121,000/ (1.1)2= $100,000

• then no adjustment is needed if the payment is expected to be collected within one year of

delivering the promised goods or services.

C. Consideration payable to customer

• Pay cash consideration to provide incentive for the customer to continue purchasing from the

enterprise.

• If a company wants to provide coupons for the customers, the enterprise will have to estimate

the amount of coupon redemptions and deduct it from the transaction price of the detergent

sold to the distributor.

find more resources at oneclass.com

find more resources at oneclass.com

• Company would then later record the consequence of the coupon

o E.g. SuperClean sells 200,000 units of laundry detergent to Best Grocery Wholesale at $3

per unit. The detergent has a manufacturing cost of $1.50 per unit and a suggested retail

price of $8. SuperClean issues 400,000 coupons for $2 each. They estimate that 30% of

coupons will be redeemed. Retailers submit claims of coupon collected amounting to

$250,000:

D. Variable Consideration

• Consideration is considered variable whenever there’s soe uertait oer aout of

consideration involved.

• Coupon example ^ can also be variable consideration because the final net amount received was

dependent on the rate of coupon redemptions.

• Volume discounts is also variable. When company offers discount if customers purchase more

than a specified number of units in the year.

e.g. BQB has a selling price of $100 a unit. It offers 10% discount if a retariler purchases at least

500 units a year. In the first half of the year, retailer X purchased 200 units. In the second half,

retailer X purchased 400 units.

• Estimating amount of variable consideration should use one of two methods:

o The expected value, which involves applying probability to possible outcomes

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

An overview of revenue recognition: criteria for revenue recognition is revenue from contracts with customers (written, verbal, formal). The standard covers any contract with a customer- a counterparty that has contracted to obtain goods or service from the reporting entity: exclusions: Trade- in old car estimated to be ,500 and pay another. Superclean sells 200,000 units of laundry detergent to best grocery wholesale at per unit. The detergent has a manufacturing cost of . 50 per unit and a suggested retail price of . They estimate that 30% of coupons will be redeemed. Retailers submit claims of coupon collected amounting to. When company offers discount if customers purchase more than a specified number of units in the year. e. g. bqb has a selling price of a unit. It offers 10% discount if a retariler purchases at least. In the first half of the year, retailer x purchased 200 units.