AFM291 Chapter Notes - Chapter 13: Accounts Receivable, Retained Earnings, Income Statement

28 Jun 2018

School

Department

Course

Professor

Notice the two entries required.

-

Accumulated Other Comprehensive Income (AOCI)

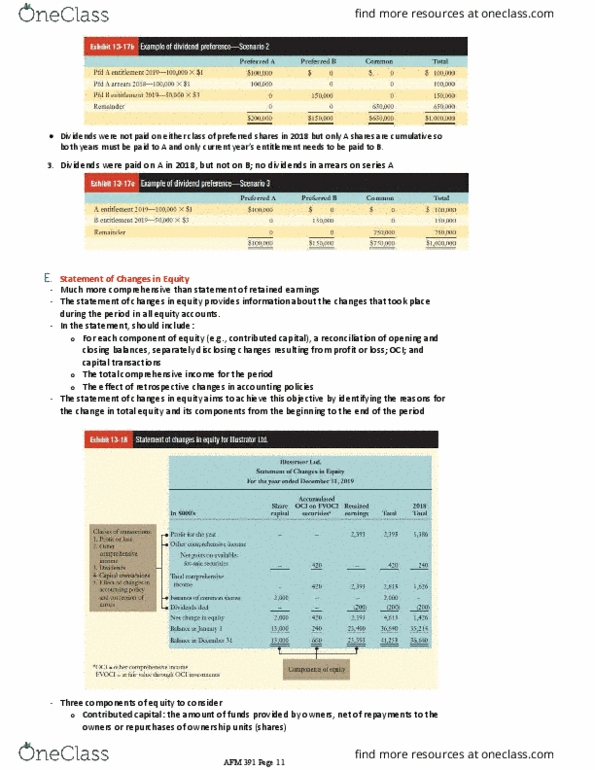

3.

ASPE doesn’t use it tho cuz aspe is dumb

o

AOCI accumulates other comprehensive income (OCI) from all prior periods like how realized

profits and losses are accumulated in retained earnings and is part of the equity section of the

balance sheet

-

IFRS uses reserves to refer to AOCI, but also other reserves like contributed surplus

-

FVOCI bond goes from 25,000 to 27,000 in market value: $2,000 unrealized gain is booked

to OCI and then its closed into AOCI at year end when closing

o

OCI represents unrealized change in the fair market value of select assets including FVOCI

investments

-

It is “parked” in AOCI

o

OCI usually does not go through net income and is not taxed

o

Recognizing amounts through OCI

Accumulating OCI in AOCI

Recognizing them in net income and retained earnings

Recycling is just the cycle of OCI

o

Recycling of OCI: the process of recognizing amounts through OCI accumulating that OCI in

AOCI (reserves), and later recognizing those amounts through net income and retained earnings

-

OCI from investment in debt securities is recycled through net income and retained earnings

-

Entity may reclassify AOCI directly to retained earnings

OCI from investments in equity securities is not

-

Journal entry debiting AOCI and crediting retained earnings thus bypassing the income

statement

2,000 is recognized to OCI

o

2,000 from OCI is closed into AOCI

o

1,000 is recognized as net income when sold and 2,000 is recycled through AOCI and

recognized as net income as well

o

Ex. FVOCI bond goes from 25,000 to 27,000 and then next year is sold for 28,000

-

Company needs to distinguish AOCI from FVOCI investments (debt) separately from amounts

arising from revaluation (equity)

-

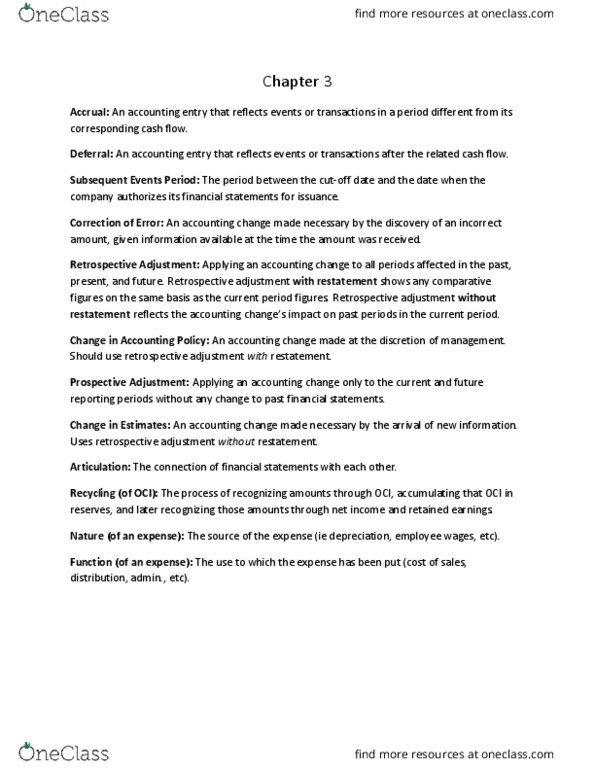

Summary

Summary of the accounting classification of different components and sub-components of

equity:

-

AFM 391 Page 3

Document Summary

Aoci accumulates other comprehensive income (oci) from all prior periods like how realized profits and losses are accumulated in retained earnings and is part of the equity section of the balance sheet. Aspe doesn"t use it tho cuz aspe is dumb. Ifrs uses reserves to refer to aoci, but also other reserves like contributed surplus. Oci represents unrealized change in the fair market value of select assets including fvoci investments o. Fvoci bond goes from 25,000 to 27,000 in market value: ,000 unrealized gain is booked to oci and then its closed into aoci at year end when closing. Recycling of oci: the process of recognizing amounts through oci accumulating that oci in. Aoci (reserves), and later recognizing those amounts through net income and retained earnings o o o o. Oci usually does not go through net income and is not taxed. Recognizing them in net income and retained earnings.